Ever wondered why the crypto market can swing wildly, yet some folks still sleep soundly at night? They’ve discovered the not-so-secret weapon: stablecoins. While Bitcoin and Ethereum play rollercoaster with your emotions, stablecoins just… chill. If you’re curious about how stablecoins work, or simply want to get a grip on stablecoin mechanisms explained, you’re about to find out why these digital assets are the calm in crypto’s storm.

Let’s cut through the noise and get you actually understanding what stablecoins are and why they might be your portfolio’s new best friend.

Stablecoins represent the calm in crypto’s storm – digital assets specifically designed to maintain a steady value by pegging themselves to real-world currencies or commodities. No more waking up to find your investment worth half what it was yesterday.

But here’s where it gets interesting: not all stablecoins are created equal. Some are backed by cold, hard cash while others use… well, let’s just say more creative methods. If you’re curious about the mechanics behind these differences, this breakdown offers a solid explainer on yield-bearing versus traditional stablecoins.

Understanding Stablecoins: The Backbone of Crypto Stability

What Are Stablecoins and Why They Matter in Today’s Market

Imagine this: you’re riding the crypto rollercoaster when suddenly your Bitcoin drops 20% overnight. Stomach-churning, right? That’s precisely where stablecoins come in—they’re the chill, level-headed friends in the wild crypto party, and a prime example of stablecoins explained thoroughly in action.

Stablecoins are cryptocurrencies designed to maintain a steady value by pegging themselves to stable assets like the US dollar, gold, or other fiat currencies. Unlike their volatile cousins Bitcoin and Ethereum, they aim to keep their cool at a consistent price point. At their core, how stablecoins work is all about maintaining balance through strategic asset backing and mechanisms that minimize volatility.

Why should you care? In 2025’s crypto landscape, stablecoins have become absolutely crucial. They offer a safe harbor when markets go wild, let you move money instantly without converting back to fiat, and serve as the backbone for DeFi lending, borrowing, and yield farming.

The numbers don’t lie – stablecoins now account for over $300 billion in market cap, with daily transaction volumes often exceeding traditional cryptocurrencies during market turbulence.

For traders, they’re the perfect pit stop between trades. For businesses, they’re a gateway to blockchain without the volatility headache. And for folks in countries with unstable currencies? They’re sometimes the only reliable money around.

How Stablecoins Differ from Traditional Cryptocurrencies

The main difference? It’s all about that price action, baby.

Bitcoin and other traditional cryptos are like untamed mustangs – free to roam up and down in value based on market sentiment. One tweet from a tech billionaire and your portfolio might soar or crash.

Stablecoins, meanwhile, are more like well-trained horses with blinders on – they’ve got one job: maintain that $1 peg (or whatever asset they’re tied to).

Here’s how they stack up:

| Feature | Traditional Cryptocurrencies | Stablecoins |

|---|---|---|

| Price behavior | Highly volatile | Steady and predictable |

| Primary use | Speculation, store of value | Medium of exchange, temporary safe haven |

| Supply mechanism | Often fixed or algorithmically controlled | Typically expands/contracts with demand |

| Backing | Generally none (pure market value) | Collateral (fiat, crypto, commodities) or algorithms |

| Risk profile | High risk, high reward | Lower risk, lower reward |

Traditional cryptos try to reinvent money. Stablecoins are just trying to make existing money work better on the blockchain.

And the tech behind them? While Bitcoin uses pure proof-of-work consensus, stablecoins employ various mechanisms—from simple dollar reserves to complex algorithmic balancing acts—all aimed at that sweet, sweet stability. If you’ve ever asked yourself how stablecoins work under the hood, this is where the magic (and math) happens.

The Evolution of Stablecoins: From Concept to Mainstream Adoption

The stablecoin story begins around 2014 with early experiments like BitUSD, but things didn’t really kick off until Tether (USDT) gained traction in 2017.

Historically, stablecoins were mostly just pit stops for traders. Nobody was talking about them at dinner parties. Fast forward to 2025, and they’ve completely transformed how we think about money on the blockchain—marking a pivotal shift in the science of stablecoins and their cultural relevance in the digital economy.

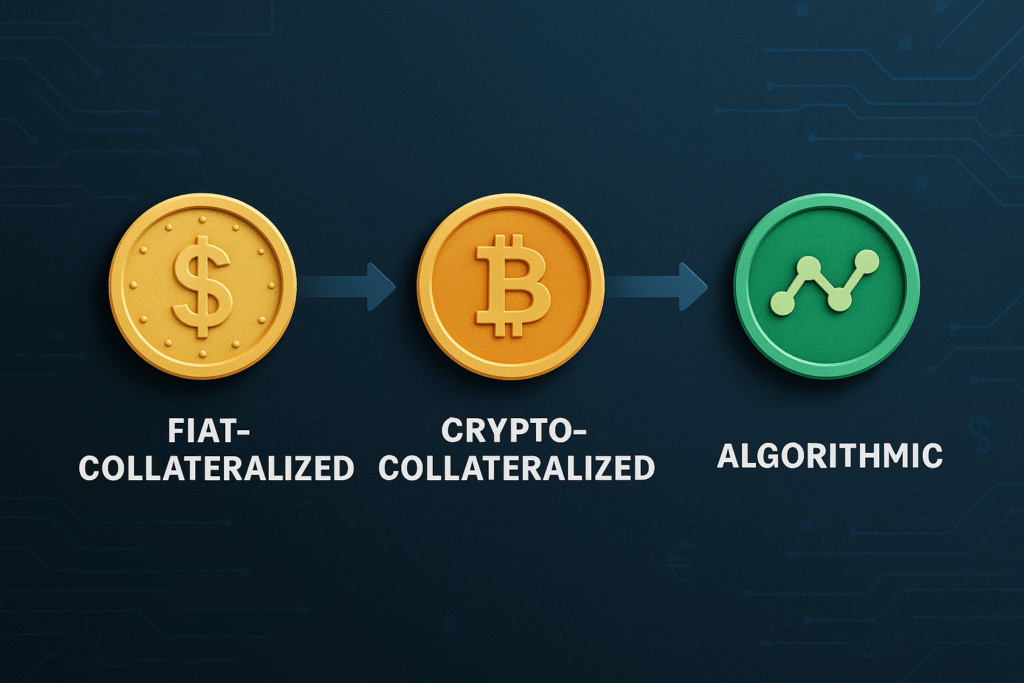

The evolution happened in distinct waves:

First came the collateralized stablecoins backed by fiat (Tether, USDC), which still dominate the market. But they had a problem – centralization and the need to trust the issuer actually had those dollars.

Then came crypto-collateralized options like DAI, which used other cryptocurrencies as backing. More decentralized, but less efficient.

The algorithmic stablecoin boom came next – coins that maintained their peg through smart contract magic rather than collateral. Remember Terra/UST’s spectacular collapse in 2022? That painful lesson led to the hybrid models we see thriving today.

Today, we’re in the era of regulated, bank-issued stablecoins. JPMorgan’s JPM Coin and major central bank digital currencies (CBDCs) have blurred the line between traditional finance and crypto—offering a new perspective on how stablecoins work when backed by institutions and embedded within legacy financial systems.

What started as a niche tool for crypto traders has evolved into infrastructure that powers everything from cross-border payments to the $1 trillion DeFi economy.

Key Benefits of Using Stablecoins in Your Investment Strategy

Smart investors don’t just use stablecoins – they weaponize them. Here’s how you can too:

Volatility shield: When markets get spicy, park your gains in stablecoins instead of cashing out completely. You stay in the crypto ecosystem, avoid potential tax events, and remain ready to pounce when opportunities arise.

Yield farming: Even in 2025, stablecoins still offer better interest rates than traditional banks. Lending platforms are paying 5-12% APY on stablecoins – that’s literally making your stable money work for you.

Dollar-cost averaging: Set up automated stablecoin purchases of your favorite volatile cryptos. This strategy smooths out your entry points and helps you sleep better at night.

Arbitrage opportunities: Different exchanges sometimes price assets differently. Stablecoins let you quickly move funds between platforms to capitalize on these differences without worrying about price slippage during transfers.

Global accessibility: Unlike traditional banking, stablecoins work 24/7 and cross borders in minutes, not days. This global liquidity is a game-changer for international investors.

Inflation hedge: For those in countries with unstable currencies, dollar-pegged stablecoins offer protection against local inflation without the volatility of Bitcoin.

The bottom line? Stablecoins aren’t just for crypto newbies scared of volatility. They’re sophisticated tools that, when used strategically, can significantly enhance returns while reducing overall portfolio risk.

The Major Types of Stablecoins Explained

A. Fiat-Collateralized Stablecoins: The Traditional Approach

The OGs of the stablecoin world? Fiat-collateralized coins.

These are the straightforward kids on the block—for every stablecoin issued, there’s an actual dollar (or euro, yen, etc.) sitting in a bank account somewhere. Think of them as digital IOUs. It’s the simplest version of how stablecoins work: one coin, one real-world asset, full stop.

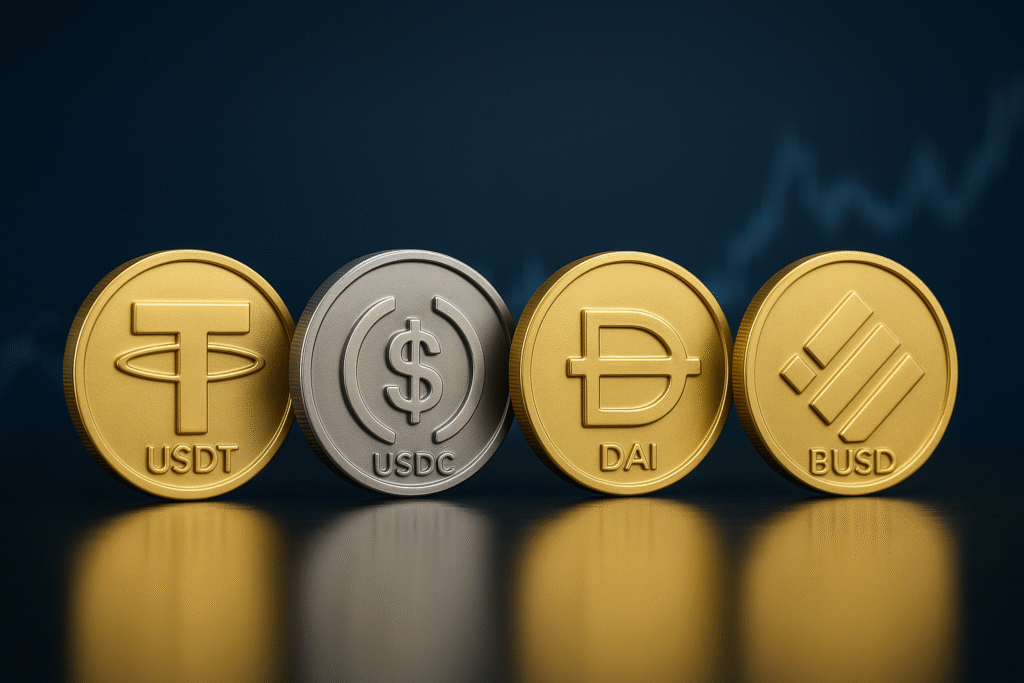

USDT (Tether) and USDC lead this pack, with billions in circulation. The math is simple: 1 USDT = 1 USD. No fancy algorithms, no complex mechanisms.

But here’s the catch – you’re trusting a central entity to actually hold those reserves. Remember when Tether got into hot water about their reserves? Yeah, that happened.

The pros are massive though:

- Minimal price volatility (usually within 1% of the peg)

- Easy to understand (even your grandma could get it)

- High liquidity in most markets

The real-world applications are already everywhere. Remittances, trading pairs on exchanges, and safe havens during market turbulence.

B. Crypto-Collateralized Stablecoins: Leveraging Blockchain Assets

Want to stay 100% in crypto while enjoying stability? Crypto-collateralized stablecoins have entered the chat.

These bad boys use other cryptocurrencies as collateral. DAI is the poster child here – backed by ETH, WBTC, and other assets locked in smart contracts.

The twist? They’re over-collateralized. You might need to put up $150 worth of ETH to get $100 worth of stablecoins. This buffer helps absorb market volatility.

When ETH price tanks? Automatic liquidation mechanisms kick in to protect the peg.

What makes these puppies special:

- Fully on-chain and transparent

- No central authority (decentralization for the win!)

- Anyone can verify the collateral in real-time

The downside? They’re less capital efficient. Locking up more value than you get out seems wasteful to some, but it’s the price of decentralized stability.

C. Algorithmic Stablecoins: How They Maintain Value Without Collateral

No collateral? No problem! Algorithmic stablecoins are the daredevils of the crypto world.

It’s like having a robot central banker who never sleeps.

Examples include Ampleforth (AMPL) and the infamous Terra UST (RIP).

The appeal is undeniable:

- No collateral requirements = capital efficiency

- Fully algorithmic = no human intervention

- Potentially unlimited scalability

But man, these have had some spectacular failures. Terra’s UST collapse in 2022 wiped out $40+ billion in value practically overnight. The “death spiral” risk is real when confidence evaporates.

Despite the risks, developers keep trying new approaches. The holy grail of a truly decentralized, uncollateralized stablecoin is just too tempting to ignore.

D. Commodity-Backed Stablecoins: Gold, Oil, and Beyond

Crypto meets the oldest money in the world with commodity-backed stablecoins.

These tokens are backed by physical assets like gold, silver, oil, or even real estate. Paxos Gold (PAXG) and Tether Gold (XAUT) are leading examples, with each token representing one fine troy ounce of gold.

What’s awesome about them:

- Protection against both crypto AND fiat inflation

- Familiar backing that traditional investors understand

- Actual physical redemption (in some cases)

The downsides aren’t trivial though. There’s custody risk (someone has to store that gold), potential regulatory hurdles, and slightly more price volatility than fiat-backed options. These challenges are part of how stablecoins work—especially when backing involves physical assets or decentralized mechanisms.

Still, for those worried about money printing and currency debasement, these offer a compelling bridge between traditional store-of-value assets and crypto’s efficiency.

E. Hybrid Models: Combining Multiple Stability Mechanisms

Why pick just one approach when you can have the best of all worlds?

Hybrid stablecoins combine multiple stability mechanisms for added resilience. Reserve might use both fiat collateral AND algorithmic controls. Frax employs a fractional-algorithmic approach with part USDC backing and part algorithmic.

These models can:

- Adjust collateralization ratios dynamically

- Implement multiple fallback mechanisms

- Scale more efficiently than pure-collateral models

The complexity makes them harder for average users to understand, but the added safety nets make them increasingly popular.

As the stablecoin market matures, these hybrid approaches may well become dominant – borrowing the best features from each model while mitigating the worst downsides.

Top Stablecoins in the Market Worth Knowing

Top Stablecoins in the Market Worth Knowing

A. USDT (Tether): The Pioneer and Market Leader

Tether blazed the trail for stablecoins back in 2014, and it’s still the big boss in the space. With a market cap that dwarfs its competitors, USDT accounts for most stablecoin trading volume worldwide.

What makes Tether tick? It’s supposedly backed 1:1 by US dollars and equivalents. But that’s where the drama starts. The company behind Tether has faced endless questions about whether they actually have all those dollars in reserve. In 2021, they settled with the New York Attorney General for $18.5 million over reserve discrepancies.

Still, crypto traders don’t seem to care much. USDT remains their go-to safe haven during market volatility. When you need to park your crypto gains somewhere or wait out a storm, Tether is typically the first choice—a testament to how stablecoins work as reliable buffers in turbulent markets.

Its widespread adoption is its superpower. Almost every exchange supports it, and it runs on multiple blockchains including Ethereum, Tron, and Solana – giving users flexibility in transaction speeds and fees.

B. USDC: The Regulated Alternative

USDC stepped into the scene in 2018 as the “we-play-by-the-rules” stablecoin. Created by Circle and Coinbase, USDC makes transparency its whole personality.

Unlike its more secretive cousin Tether, USDC publishes monthly attestations that confirm its dollar reserves. This approach has won it fans among institutions and businesses that need compliance boxes checked.

The downside? It’s still largely centralized. Circle can freeze addresses if required by law, which makes crypto purists squirm.

C. DAI: The Decentralized Option

DAI flips the stablecoin script entirely. Instead of a company holding dollars in a bank, DAI is generated through crypto collateral locked in smart contracts.

Created by MakerDAO, DAI maintains its dollar peg through a complex system of over-collateralization. Users deposit crypto assets worth more than the DAI they want to generate – typically at least 150% of the value.

What happens if your collateral drops too low? The system liquidates it. Harsh but effective for keeping DAI stable.

The beauty of DAI is its resistance to censorship. No single entity can freeze your funds or shut down the system. It’s stablecoin money for the crypto idealists.

The trade-off is complexity. Creating DAI requires understanding collateral ratios, stability fees, and liquidation mechanics – not exactly beginner-friendly stuff.

D. BUSD and Other Exchange-Backed Stablecoins

Exchange-backed stablecoins like BUSD (Binance USD) represent crypto exchanges throwing their hats into the stablecoin ring.

BUSD was Binance’s answer to the stablecoin question – a regulated dollar-pegged token created in partnership with Paxos. However, in 2023, regulatory pressure forced Paxos to stop issuing new BUSD, showing how quickly fortunes can change in this space.

Other exchanges have their own versions:

| Exchange | Stablecoin | Key Feature |

|---|---|---|

| Gemini | GUSD | Fully regulated in NY |

| FTX | USDⓈ | Exchange-only utility |

| Huobi | HUSD | Multi-collateral backing |

Exchange stablecoins often come with perks on their native platforms—lower trading fees, higher yields, or special access to products. The catch? You’re putting a lot of trust in that exchange’s financial health and compliance practices. It’s a trade-off baked into how stablecoins work when issued and managed by centralized crypto platforms.

Practical Applications of Stablecoins in Today’s Economy

Cross-Border Transactions: Faster and Cheaper Alternatives

Remember when sending money overseas meant waiting days and paying ridiculous fees? Stablecoins have completely changed the game. Unlike traditional bank transfers that can take 3-5 business days and charge up to 7% in fees, stablecoin transfers happen in minutes and cost pennies.

Take Maria in Chicago sending $500 to her cousin in Mexico City. With a traditional wire transfer, she’d pay around $25-45 in fees and her cousin would wait days. Using USDC or USDT stablecoins, she pays less than $1 in network fees, and her cousin receives the full amount almost instantly.

Major companies like Visa and Mastercard aren’t sitting on the sidelines either. They’ve integrated stablecoin settlement into their back-end systems to speed up their own cross-border payment networks—an enterprise-level example of how stablecoins work to streamline global financial infrastructure.

DeFi Opportunities: Lending, Borrowing, and Yield Farming

Stablecoins are basically the backbone of decentralized finance. No joke.

On platforms like Aave and Compound, you can lend your stablecoins and earn anywhere from 2-8% APY – way better than the 0.01% your bank offers. And unlike traditional finance, there’s no minimum amount or lengthy application process.

Many DeFi users practice “yield farming” by moving their stablecoins between different protocols to maximize returns. A simple strategy might look like:

| Platform | Strategy | Potential Yield |

|---|---|---|

| Curve Finance | Provide liquidity to stablecoin pools | 3-5% base APY |

| Yearn Finance | Auto-compounding vaults | 5-15% APY |

| Convex | Boosted Curve yields | Additional 2-5% |

The best part? You maintain control of your assets the entire time, with no lockup periods or permission needed.

Everyday Payments and E-Commerce Integration

In June 2025, over 75,000 merchants worldwide now accept stablecoin payments. Big names like Shopify have built-in USDC payment options, letting online stores receive payments without the typical 2-3% credit card processing fees.

The customer experience is getting smoother too. Apps like Circle and Coinbase Commerce let you pay with stablecoins by simply scanning a QR code – often faster than pulling out your credit card.

For business owners, stablecoins solve the headache of chargebacks – those disputed transactions that cost merchants billions each year. Stablecoin transactions are final, with no risk of the dreaded “friendly fraud” where customers make purchases then falsely claim they never received the item.

Remittances: Helping Families Across Borders

The remittance industry has been ripping people off for decades. Migrant workers sending money home lose an average of 6.5% to fees and terrible exchange rates. That’s a $45 billion annual tax on some of the world’s hardest workers.

Stablecoins flip this model upside down. Filipino workers in Dubai are now using USDC to send money home, saving about $14 on every $200 transfer. The money arrives in minutes, not days.

Real-world impact? A construction worker sending $800 monthly can save nearly $600 yearly – enough for a family member’s school fees or medical expenses back home.

Companies like Tala and Coins.ph have built user-friendly mobile apps specifically for these remittance corridors, making the technology accessible even to people with limited tech experience.

Hedging Against Market Volatility

When crypto markets go wild, stablecoins become digital safe houses.

During the last market crash in early 2025, trading volumes for USDT and USDC hit all-time highs as traders rushed to preserve their gains or limit losses. Unlike selling to fiat (which can take days to withdraw), converting to stablecoins takes seconds.

Smart traders use stablecoins strategically:

- During bull markets: Taking partial profits into stablecoins

- During bear markets: Building a “dry powder” reserve for buying opportunities

- Always: Keeping an emergency fund that won’t fluctuate in value

For people in countries with unstable currencies, stablecoins offer protection from local inflation. Venezuelans and Argentinians were early adopters for this exact reason—when your national currency loses 10% of its value monthly, a dollar-pegged stablecoin becomes a financial lifeline. It’s a stark, real-world example of how stablecoins work to preserve value in the face of economic instability.

Regulatory Landscape and Future Outlook

Current Regulatory Approaches Across Major Jurisdictions

The regulatory landscape for stablecoins is wildly fragmented in 2025. Each major jurisdiction has taken its own path:

United States: After years of debate, the U.S. finally passed the “Digital Asset Market Structure Act” in late 2024, creating a comprehensive framework specifically for stablecoins. Issuers must now maintain 100% reserves in high-quality liquid assets and undergo quarterly audits. This regulatory clarity reshapes how stablecoins work, adding trust and transparency to their operational core.

European Union: The Markets in Crypto-Assets (MiCA) regulation is fully implemented, classifying stablecoins as “e-money tokens” or “asset-referenced tokens” with strict reserve requirements and consumer protections.

Singapore: The Monetary Authority of Singapore (MAS) has created a regulatory sandbox specifically for stablecoin projects, balancing innovation with stability through a principles-based approach.

China: Meanwhile, while CBDC development continues aggressively with the e-CNY, private stablecoins remain effectively banned—highlighting the geopolitical tension within mastering stable digital currencies and who gets to control them.

The global picture? A regulatory patchwork that has stablecoin issuers scrambling to adapt.

Compliance Challenges and How Projects Are Addressing Them

Stablecoin projects face mounting compliance hurdles:

Cross-border operations: Managing different regulatory requirements across jurisdictions is like playing regulatory whack-a-mole.

Reserve transparency: Many projects now employ real-time attestation technology using blockchain oracles to provide continuous verification of reserves, moving beyond traditional quarterly audits.

KYC/AML implementation: Projects like Circle (USDC) have deployed sophisticated on-chain analytics to identify suspicious transactions while preserving user privacy.

Governance structures: DAOs are evolving to include regulatory compliance committees with legal experts to ensure protocols remain compliant despite decentralized governance.

The compliance burden is heavy, but it’s driving surprising innovation. Tether has increased transparency—publishing treasury-backed attestations—and institutions across finance are ramping up AI‑driven RegTech solutions.

Central Bank Digital Currencies (CBDCs) vs. Private Stablecoins

The relationship between CBDCs and private stablecoins has evolved from competition to coexistence:

| Feature | CBDCs | Private Stablecoins |

|---|---|---|

| Issuer | Central banks | Private companies/DAOs |

| Programmability | Limited (by design) | Highly flexible |

| Privacy | Varies by jurisdiction | Varies by design |

| Cross-border use | Typically limited | Global by default |

| Innovation pace | Slow, deliberate | Rapid |

CBDCs have gained traction in 11 major economies, with China’s e-CNY leading adoption. But they haven’t killed private stablecoins as many predicted. Instead, we’re seeing specialization:

CBDCs dominate retail payments in some regions, while private stablecoins thrive in DeFi, cross-border transactions, and regions with currency instability—each use case showcasing how stablecoins work across a spectrum of economic environments and financial infrastructures.

The most interesting development? The emergence of “hybrid models” where private stablecoins are built atop CBDC infrastructure but add programmability layers.

Predictions for Stablecoin Adoption in the Next Five Years

Stablecoin adoption is accelerating beyond crypto enthusiasts. Here’s what’s coming:

Mainstream financial integration: By 2027, major banks may begin offering stablecoin-based services to customers. JPMorgan is exploring this space—though its efforts currently focus on internal infrastructure, not USDC partnerships.

Cross-border commerce revolution: As a result, international e-commerce platforms will increasingly offer stablecoin payment options, reducing forex fees and settlement times. It’s a real-world evolution of stablecoin insights and strategies—as frictionless, borderless digital money built for global commerce.

Specialized stablecoins: We’ll see more purpose-built stablecoins optimized for specific use cases – from gaming economies to decentralized insurance.

Algorithmic comeback: After the Terra/Luna collapse, algorithmic stablecoins disappeared. They’re returning with hybrid designs that combine collateral with algorithmic stability mechanisms.

Institutional reserves: The most controversial prediction? Some smaller nation-states will begin holding stablecoins as part of their foreign currency reserves by 2029.

The stablecoin market cap will likely grow from today’s $267 billion to over $1 trillion by 2030, driven by real-world utility rather than speculation.

Risks and Considerations Before Investing

A. Counterparty Risk: Understanding Who Backs Your Coins

Ever wonder who’s actually holding your money when you buy stablecoins? That’s counterparty risk in a nutshell.

When you own USDC or USDT, you’re basically trusting Circle or Tether to actually have the dollars they claim. If they don’t? Your “stable” coin might be worth nothing overnight.

Take the 2022 Terra/Luna collapse. Billions vanished because the algorithm couldn’t maintain the peg. Or consider Tether’s sketchy history with audits. For years they promised full backing but kept changing their story about what actually backed their tokens.

Smart investors check:

- Regular, comprehensive audits from reputable firms

- Clear transparency about reserves (not vague promises)

- The jurisdiction where the company operates

- Their track record during previous market crashes

B. Smart Contract Vulnerabilities and Technical Risks

The code running your stablecoins isn’t bulletproof.

Remember the 2016 DAO hack? One recursive flaw, and $60 million in ETH vanished. Fast-forward to today, and smart contract exploits haven’t slowed down—they’ve just gotten more sophisticated. In 2022, Wormhole lost $325 million. In 2023, Euler Finance bled $200 million. These aren’t edge cases—they’re warnings. Smart contracts may power your favorite stablecoins, but under the hood, they’re ticking time bombs unless rigorously audited and constantly monitored.

Common technical risks include:

- Oracle failures (when price feeds malfunction)

- Admin key compromises (when privileged accounts get hacked)

- Flash loan attacks (manipulating prices through massive temporary loans)

- Governance attacks (when token voting systems get hijacked)

The best protocols undergo multiple security audits and have bug bounty programs. Still, even audited code isn’t guaranteed safe.

C. De-Pegging Events: When Stablecoins Become Unstable

Stablecoins don’t always stay stable. Shocking, right?

Consequently, de-pegging happens when market forces overwhelm the mechanisms keeping a stablecoin at $1. During the 2022 crypto crash, even USDT briefly dipped to $0.95 on some exchanges—a stark reminder of the fragility behind how stablecoins function under pressure.

What causes de-pegging? Usually panic. When everyone rushes for the exit at once, redemption mechanisms get overwhelmed. The price falls, triggering more panic selling in a nasty spiral.

For algorithmic stablecoins, it’s even worse. Just ask anyone who held UST when it collapsed from $1 to pennies in days. That’s not a “dip” – that’s financial obliteration.

How to protect yourself:

- Diversify across different stablecoin types

- Monitor on-chain metrics for warning signs

- Have exit strategies ready

- Never keep more in stablecoins than you can afford to lose

D. Liquidity Concerns in Different Market Conditions

Liquidity is like oxygen for your investments – you only notice when it’s gone.

During calm markets, trading $100K of USDC barely moves the price. But when markets panic? That same trade might cost you significant slippage.

Each stablecoin type has different liquidity profiles:

- Fiat-backed coins (USDC, USDT) typically maintain best liquidity

- Crypto-collateralized coins (DAI) face pressure during major market dumps

- Algorithmic stablecoins often collapse completely in liquidity crises

Remember March 2020? Markets went into overdrive as everyone fled to cash—bond and money-market spreads widened dramatically. While stablecoins escaped the worst of the chaos, traders on crypto exchanges did see spot-spread spikes that wiped out weeks of yield in seconds.

Always check:

- Trading volume across multiple exchanges

- Bid-ask spreads in normal conditions

- Historical behavior during previous crashes

- Redemption limitations or waiting periods

E. Tax Implications of Stablecoin Transactions

The taxman doesn’t care that your stablecoins stayed at $1. He still wants his cut.

Despite their “stable” nature, most tax authorities treat stablecoin transactions as taxable events. Think you’re safe because the price didn’t change? Think again. This quirk in regulation reflects how stablecoins work in practice—stable in value, but not always in treatment.

In the US, every stablecoin-to-stablecoin swap is potentially reportable. Those “tax-free” interest earnings on lending platforms? They’re probably taxable income.

The pain points get worse:

- Staking rewards are typically taxable when received

- Lending interest creates taxable events

- Moving between stablecoins creates reporting requirements

- Some DeFi activities generate taxable events with every block

Furthermore, tax reporting tools help, but they’re imperfect. Miss transactions and you risk audits or penalties. Some jurisdictions might even classify certain stablecoins differently than others—adding another layer of complexity to stablecoin mechanisms explained and how they’re treated across borders.

Keep meticulous records. Document every transaction. And please, talk to a crypto-savvy tax professional before assuming anything is tax-free.

Getting Started with Stablecoins: A Practical Guide

Choosing the Right Stablecoin for Your Needs

Picking a stablecoin isn’t a one-size-fits-all deal. Your choice should match what you’re trying to do with it.

If you’re looking for something rock-solid and widely accepted, USDC and USDT are your go-to options. Both are pegged to the US dollar and available on practically every exchange out there. USDC has a slight edge in transparency, with regular audits of its reserves.

For the privacy-conscious crowd, DAI stands out. It’s decentralized and doesn’t require KYC verification to use. The tradeoff? Slightly higher transaction fees compared to centralized options.

Planning to send money internationally? BUSD might be your best bet with its lower cross-border transfer fees.

Here’s a quick breakdown:

| Stablecoin | Best For | Backed By | Network Fees |

|---|---|---|---|

| USDC | General use, US users | USD reserves | Low-Medium |

| USDT | Trading, liquidity | Mixed reserves | Low |

| DAI | Privacy, decentralization | Crypto collateral | Medium-High |

| BUSD | International transfers | USD reserves | Low |

| USDC | General use, US users | USD reserves | Low-Medium |

Got DeFi ambitions? Look at DAI or FRAX for their solid integration with lending platforms and yield farming.

Best Exchanges and Wallets for Stablecoin Transactions

Your stablecoin experience is only as good as where you keep them and trade them.

In addition, for exchanges, Coinbase Pro offers fee-free USDC transactions, making it perfect if that’s your stablecoin of choice. Binance takes the crown for variety, supporting nearly every major stablecoin with decent liquidity—a practical perk when navigating understanding stablecoins in real-world trading environments.

If fees make you cringe, check out Kraken’s stablecoin pairs with some of the lowest trading fees in the business. It’s a savvy example of how stablecoins work to streamline costs and boost efficiency in crypto trading.

Hardware wallet fans should look at Ledger or Trezor – both support the major stablecoins and keep your assets off exchanges.

For day-to-day use, MetaMask remains the gold standard for DeFi interactions. Just remember to connect it to the right network to avoid those painful gas fees on Ethereum.

Mobile users can’t go wrong with Trust Wallet or Exodus, both offering clean interfaces and solid security.

Quick tip: Always double-check the network when withdrawing stablecoins from exchanges. Sending USDC on Ethereum instead of Solana could cost you an extra $20 in fees!

Security Best Practices for Stablecoin Holdings

Stablecoins might be stable in price, but they’re not immune to security risks.

First things first: Never share your private keys or seed phrases. Not with support staff, not with that friendly stranger in your DMs, not with anyone. Write them down on paper and store them somewhere safe – preferably in multiple locations.

Moreover, two-factor authentication isn’t optional anymore. Enable it everywhere: exchanges, web wallets, even your email accounts. Use an authenticator app rather than SMS when possible—especially if you’re engaging deeply with the science of stablecoins and want to keep your digital assets secure.

Hardware wallets aren’t just for Bitcoin whales. Even modest stablecoin holdings deserve that extra protection. Consider it insurance for your digital dollars.

Watch those smart contract interactions. When connecting your wallet to DeFi protocols, always verify the website URL and contract addresses. Fake websites with identical looks but malicious code are everywhere in crypto.

Consider using a separate device just for crypto transactions. That old phone gathering dust? Wipe it clean, install only essential wallet apps, and you’ve got yourself a crypto-specific device that’s less likely to get compromised.

Tracking and Managing Your Stablecoin Portfolio

Staying on top of your stablecoin holdings doesn’t have to be complicated.

Portfolio trackers like CoinStats, Delta, or FTX (formerly Blockfolio) connect to your wallets and exchanges to give you a bird’s-eye view of your assets. Most importantly, they’ll help you track your tax obligations – because yes, stablecoin trades count as taxable events in most countries.

Speaking of taxes, keep detailed records of all your stablecoin transactions. Tools like Koinly or Coinledger can save you hours of spreadsheet agony when tax season rolls around.

Want to earn passive income? Staking platforms like Gemini, KuCoin, or Coinbase let you lend your stablecoins for decent yields. Just remember that higher APYs usually come with higher risk.

For the spreadsheet lovers, set up a simple tracking system: date, transaction type, amount, platform, and purpose. This habit will save you countless headaches later—especially as you deepen your understanding of stablecoin operations demystified and their role in your financial moves.

Most importantly, set clear goals for your stablecoin strategy. Are they a hedge against market volatility? A way to earn yield? Understanding your “why” makes managing your portfolio much simpler.

Conclusion

Stablecoins have emerged as a critical innovation in the cryptocurrency ecosystem, offering the technological benefits of blockchain while mitigating the extreme volatility that characterizes many digital assets. As we’ve explored throughout this guide, these assets come in various forms—from fiat-collateralized to crypto-collateralized and algorithmic stablecoins—each serving unique purposes in the broader financial landscape. Whether you’re using them for trading, remittances, or as a hedge against inflation in uncertain economies, stablecoins provide practical utility that extends well beyond theoretical use cases.

Before diving into stablecoins, remember to conduct thorough research on the specific tokens you’re interested in, understand the regulatory environment in your jurisdiction, and assess the risks involved. The stablecoin market continues to evolve rapidly alongside increased regulatory scrutiny and technological advancements. By starting with small amounts and using reputable exchanges as outlined in our guide, you can confidently begin incorporating these digital assets into your financial strategy. Understanding how stablecoins work will empower you to navigate this shifting landscape as the cryptocurrency ecosystem continues its journey toward mainstream adoption. Your next money move starts here—visit the Investillect blog for more.