Investing for beginners can feel like being dropped into a foreign country without a map or translator. The jargon is dense, the risks seem huge, and everyone online is either yelling about crypto or bragging about early retirement. It’s no wonder so many people never take the first step.

But here’s the truth: you don’t need thousands of dollars, a finance degree, or a perfect strategy to start. You just need a clear, simple path—and a little confidence to take that first leap.

This guide is your blueprint. We’ll walk you through everything from defining your goals to building your first portfolio with tools anyone can use. Whether you’ve never opened a brokerage account or you’re just tired of your savings sitting idle, you’re in the right place.

✨ Fun fact: nearly 42% of Americans aren’t investing at all—meaning you’re already ahead of the curve just by showing up. (📎 Gallup poll)

Let’s get you from zero to investor. No jargon. No fluff. Just smart, actionable steps.

Getting Started with Investing for Beginners

Know Your Why

Before you invest a single dollar, you need clarity on why you’re doing it. “To make money” isn’t enough—because when the market dips or your progress feels slow, that vague goal won’t motivate you to stay the course.

Are you investing to retire early? Buy a home in five years? Build financial freedom so you can say “no” to toxic jobs? Getting specific about your “why” makes it easier to pick the right strategy and stay committed. For example, if your goal is long-term wealth, index funds might be ideal. If you’re saving for a down payment in three years, a more conservative portfolio makes sense.

Write it down. Tape it to your laptop. Make it your phone background if you have to. Your “why” is your anchor in this process.

📎 Read more on goal-based investing from Vanguard

Don’t Skip the Basics

One of the biggest mistakes beginners make? Jumping straight into stock picking without understanding the basics. It’s like trying to bake a soufflé before you’ve boiled an egg.

Take time to learn the fundamentals: What’s a stock? What’s a bond? What’s diversification, and why does it matter? You don’t need to memorize every term—but understanding how these pieces fit together helps you invest smarter and avoid big missteps.

Here’s a better alternative: Start with a solid foundation. Read a few beginner articles. Watch a YouTube breakdown on index funds. Learn what risk tolerance really means.

📎 Check out our guide on Stock Market Basics

Mastering the basics isn’t boring—it’s empowering. And it’ll save you a lot of stress (and money) down the road.

Building Your First Portfolio as a Beginner

Pick the Right Platform

Choosing the right investing platform is like picking the right gym—it should match your needs, feel intuitive, and not charge you ridiculous fees just to show up.

For beginners, user-friendly apps like Fidelity, Charles Schwab, SoFi, or Robinhood can help you dip a toe into investing without feeling overwhelmed. If you want a more hands-off experience, robo-advisors like Betterment or Wealthfront build and manage a portfolio for you based on your goals and risk level.

Start with a platform that offers:

No minimum balance or low fees

Easy-to-understand dashboards

Educational resources or tutorials

📎 NerdWallet’s top beginner platforms

Remember: you’re not marrying your first app. You’re learning the ropes—comfort matters more than complexity.

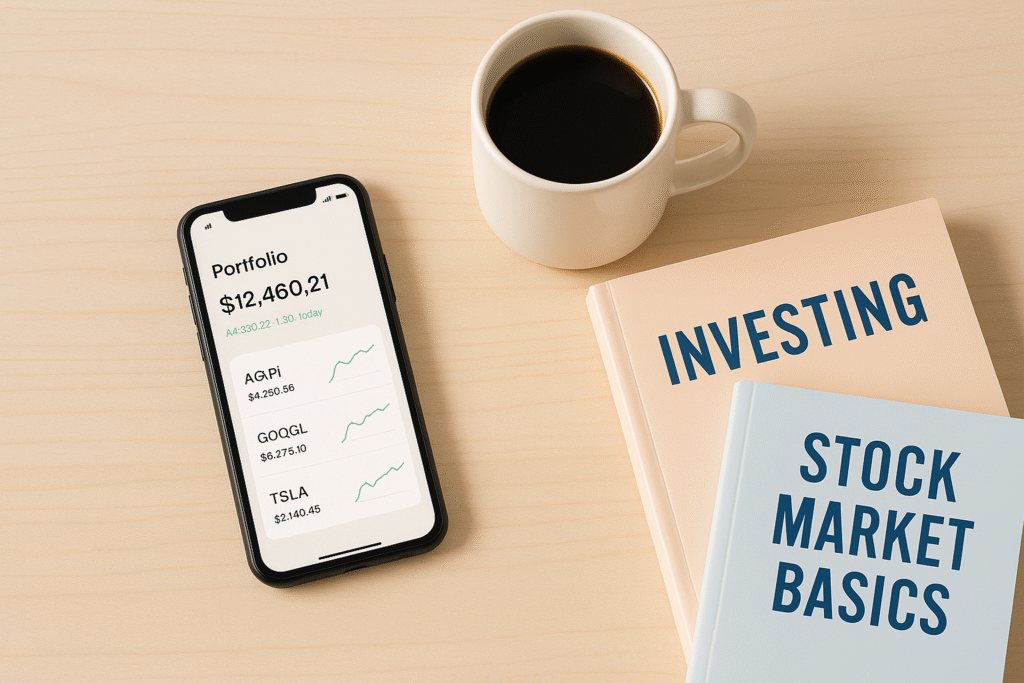

Start with ETFs or Index Funds

Forget what TikTok told you—jumping into individual stocks isn’t the best starting line. What you really want are index funds or ETFs (exchange-traded funds). Why? They’re like financial smoothies: one share includes a mix of many different companies, which spreads your risk and keeps things simple.

Think of an S&P 500 ETF (like VOO or SPY) as a starter pack of the U.S. economy. Instead of betting on one company, you’re investing in hundreds. That’s powerful for beginners who want stability and steady growth.

Start small: $10, $20, $50. Set up recurring buys so it happens automatically.

📎 Here’s a breakdown on ETFs vs. mutual funds

Bonus: most brokerages now offer fractional shares, so you don’t need $300 to buy into a fund. You just need the will to begin.

Automate It

Want to know the single easiest way to become a consistent investor? Automation. Set a recurring transfer—weekly, bi-weekly, monthly—and forget about it.

Automation takes emotion out of the equation. No more stressing over timing or trying to “buy the dip.” You’re investing steadily, no matter what the market’s doing.

Even $10/week adds up. Over time, it becomes a habit—like brushing your teeth, but for your financial future.

📎 Set up auto-investing with M1 Finance

Small moves, done consistently, beat sporadic bursts of effort every time.

Smart Strategies for Investing for Beginners

Strategy or How-To – Dollar-Cost Averaging

Timing the market is a trap—even pros get it wrong. Enter dollar-cost averaging (DCA): a simple, effective strategy where you invest a fixed amount of money at regular intervals, regardless of the market’s ups and downs.

Let’s say you invest $100 every month. When prices are low, you buy more shares. When prices are high, you buy fewer. Over time, this averages out your cost per share and helps reduce the emotional whiplash of market volatility.

This method doesn’t require any market predictions—just consistency. Most brokerage platforms let you set up auto-investing so your money moves like clockwork.

📎 Morningstar explains dollar-cost averaging

It’s simple. It’s smart. And it’s especially perfect for beginners who want to build wealth without the drama.

Know What Affects Your Returns

Fees Eat Profits

Here’s an unsexy truth about investing that’ll save you thousands: fees matter—big time.

A 1% annual fee might not sound like much, but over 30 years, it could slash your returns by tens of thousands of dollars. That’s money that should be compounding quietly in your favor, not padding a manager’s paycheck.

Let’s say you invest $10,000 and earn an average of 7% annually. With no fees, that grows to about $76,000 in 30 years. Add a 1% fee? Now it’s closer to $57,000. You just lost nearly $19,000—without doing anything wrong.

So what should beginners look for?

Stick with low-cost index funds (like Vanguard or Schwab funds with 0.03% expense ratios).

Avoid high-fee mutual funds unless you truly understand their value.

Always check the expense ratio and platform fees before you invest.

📎 Use this free fee impact calculator from the SEC

Being fee-savvy isn’t nitpicking. It’s smart strategy—and it keeps more of your money growing for you.

Avoid These Rookie Investing Mistakes

Overreacting to Market Drops

Markets don’t just go up—they dip, dive, and sometimes downright crash. And for beginners, the first red day can feel like the sky is falling. Your instinct might scream: “Sell everything before I lose it all!”

Resist that urge.

Reacting emotionally to short-term losses is one of the most expensive mistakes you can make. Historically, markets recover—and long-term investors are the ones who benefit. Selling in a panic locks in your losses and throws your plan off course.

Instead, remember your long game. If your portfolio is diversified and built around your goals, temporary dips are just noise.

📎 How to Stay Calm in a Down Market

Going All-In Too Fast

Another rookie move? Dumping all your money into investments right away—especially on a hot tip or a gut feeling.

Investing is a marathon, not a sprint. Going all-in too fast can leave you vulnerable to bad timing, poor diversification, or emotional burnout. Instead, ease in gradually. Try dollar-cost averaging. Test different platforms. Build confidence before adding more fuel.

Also: Keep an emergency fund. You don’t want to pull out of your portfolio just because your car breaks down.

Start smart. Start steady. Let time—and compounding—do the heavy lifting.

Simple Habits That Help You Grow Wealth

![]()