What if your portfolio could quietly grow itself—no constant tinkering, no timing the market, and no emotional roller coasters? That’s the promise behind Dividend Reinvestment Plans (DRIPs), one of the most underrated strategies for long-term investors. In this guide, we’ll unpack the benefits of DRIP investing—a method that automatically reinvests dividends to accelerate compounding returns. Whether you call it automatic wealth building, passive income through DRIPs, or simply reinvesting dividends, the strategy delivers consistent, low-maintenance growth.

Moreover, DRIPs are ideal for those who value discipline over hype. Instead of taking dividend payouts as cash, you let them flow back into your investment, buying additional shares and building momentum over time. This reinvestment loop works especially well in volatile markets and long-term portfolios. If you’re aiming for financial freedom without obsessing over charts and news cycles, this post is your blueprint. Let’s explore how DRIPs can work harder so you don’t have to.

📘 DRIPs Decoded: What They Are and Why They Matter

✅ What Is a Dividend Reinvestment Plan (DRIP)?

A Dividend Reinvestment Plan (DRIP) is a simple yet powerful program that lets shareholders automatically reinvest their cash dividends into additional shares—or even fractional shares—of the same stock. Rather than receiving payouts as cash, your dividends are put back into ownership, accelerating compounding growth. This is one of the prime benefits of DRIP investing, also known as automatic wealth building, reinvesting dividends, or passive income through DRIPs.

Moreover, DRIPs are usually commission‑free or come with minimal fees, and sometimes offer shares at a discounted price directly from the company. There are three common types: company‑operated DRIPs, broker‑operated DRIPs, and third‑party programs/DSPPs, each enabling steady accumulation of more shares over time while minimizing investment effort. Consequently, DRIPs invite long-term investors who prefer automated, disciplined strategies over reactive trading. Importantly, dividends reinvested via DRIPs are still taxable in most taxable accounts—but the compounding upside typically outweighs the tax impact. Flexible, low-hassle, and aligned with growth goals, DRIPs are a foundational tool for long-term investors.

📌 Discover how dividend reinvestment works on Investing.com

🔁 How DRIPs Reinvest for You

A Dividend Reinvestment Plan (DRIP) works by automatically reinvesting dividends into additional or fractional shares of the same stock you already own. This mechanism drives one of the core benefits of DRIP investing, such as passive income through DRIPs and automatic wealth building.

Here’s how DRIPs work step by step:

Dividends are issued by the company you hold shares in.

Instead of cash, the DRIP uses that dividend to purchase more stock.

Shares are bought automatically, often commission-free or even at a discount.

Reinvestment is ongoing, compounding over time with each payout.

Fractional shares are included, so every cent is reinvested efficiently.

Moreover, DRIPs eliminate the temptation to spend dividends or time the market. Consequently, they build a steady, low-maintenance portfolio.

Importantly, dividends reinvested through DRIPs are still taxable in most accounts.

📌 Dividend Reinvestment Plans (DRIPs): How They Work and Why They Matter

🔍 Types of DRIP Programs

Several types of DRIP programs cater to different investor goals—each offering unique benefits of DRIP investing, from passive income through DRIPs to enhanced cost efficiency.

Moreover, understanding these variations helps investors align their strategy with their financial goals. Consequently, choosing the right DRIP type can increase returns and reduce manual effort over time.

| Type | Description | Pros | Considerations |

|---|---|---|---|

| Company-Operated DRIPs | Run directly by the issuing company. | Often commission-free, may offer discounted shares. | May require direct enrollment paperwork. |

| Third-Party DRIPs | Managed by a transfer agent or external provider. | Easy administration, still automatic. | May include small service fees. |

| Brokerage (Synthetic) DRIPs | Offered through investment brokers using open market purchases. | Seamless, flexible across multiple stocks. | No discounts, prices may vary slightly. |

| Direct Stock Purchase Plans (DSPPs) | Lets you buy stock directly from the company and enroll in DRIPs. | Combine direct buying and automatic reinvestment. | May have minimum investment requirements. |

🌱 Compounding in Action

DRIPs bring the true magic of compound growth to life—turning every dividend into fresh equity without lifting a finger. When dividends are automatically reinvested, they purchase more shares that, in turn, generate dividends themselves. This cycle illustrates the benefits of DRIP investing, passive income through DRIPs, and automatic wealth building working in tandem.

“The true power of DRIP investing isn’t the dividends you collect—it’s the wealth those reinvested dividends quietly build over time.”

Furthermore, as your share count increases over time, each dividend payout grows larger—accelerating growth in a way that reinvesting dividends alone simply cannot match. Meanwhile, market dips often mean your plan buys shares at lower prices, fueling compound returns even faster.

Importantly, compounding through DRIPs requires patience; the real power emerges over years or decades. Consequently, DRIPs reward disciplined, long-term investors with steadily compounding wealth.

📌 Learn how compound interest and reinvested dividends build wealth on Forbes

💸 The Big Benefits of DRIP Investing

💤 Wealth Without Effort

Imagine receiving income that silently compounds—dividends reinvested automatically, stacking share upon share without you lifting a finger. That’s the essence of one of the most compelling benefits of DRIP investing, including passive income through DRIPs, automatic wealth building, and consistent reinvesting dividends—all wrapped in one seamless system.

Moreover, DRIPs are commonly commission-free or charge minimal fees, so every penny works harder. Consequently, investors avoid the friction of trade execution and the temptation to liquidate dividends impulsively.

Key reasons DRIPs build wealth without effort:

🔄 Reinvesting is automated—no manual trades required

💸 Minimal or no fees, so full dividends go to work

🧠 Emotion-free investing helps avoid market-timing mistakes

📈 Growth compounds steadily with each payout cycle

💤 Perfect for set-it-and-forget-it strategies over decades

Importantly, DRIPs reward patience. Over time, modest dividend payments evolve into real portfolio momentum.

📌 DRIP Investing Explained: How Dividend Reinvestment Builds Long-Term Wealth

🧠 Emotional Discipline

Navigating the ups and downs of the market can test even the best investors. That’s where DRIPs shine—offering true emotional discipline through automation. By automatically reinvesting dividends, you avoid second-guessing market moves, resist short-term impulses, and stay focused on long-term compounding—another core benefit of DRIP investing, supporting passive income through DRIPs, automatic wealth building, and consistent reinvesting dividends.

Furthermore, DRIPs eliminate the stress of decision-making. Your plan reinvests on schedule, no matter the market mood, helping you dodge the traps of fear and greed. Consequently, investors stay committed to their long-term strategies, free from the pressure to buy high or sell low during emotional spikes.

Importantly, this structure builds resilience. Over time, the habit of reinvesting becomes second nature, reinforcing your financial discipline with each dividend cycle. DRIPs aren’t just about gains—they’re about staying in the game.

📌 Learn how emotional investing costs you on NuWealth

🧾 Low to No Fees

One of the standout benefits of DRIP investing is notably low or no fees—a key advantage for anyone building passive income through DRIPs, automatic wealth building, or reinvesting dividends efficiently.

Most company-operated DRIPs offer commission-free reinvestment, allowing your full dividend to spin directly into additional shares. Moreover, many brokerage DRIPs do not charge transaction fees, ensuring each dollar is absorbed into share accumulation—not lost to overhead. Consequently, long-term investors benefit from compounding returns without friction.

Here’s a quick look at fee structures across DRIP providers:

| DRIP Provider Type | Fee Structure | Typical Benefit |

|---|---|---|

| Company-Operated DRIP | Usually no fees, some discounts | 100% of dividend reinvested, discounted shares |

| Third-Party Transfer Agent | May charge small service fees | Automated reinvestment with minimal effort |

| Brokerage-Operated DRIP | Typically no commissions | Seamless reinvestment across portfolios |

Importantly, keeping fees low lets compounding do the heavy lifting—boosting total returns significantly over time.

📌 What Are No-Fee DRIPs? Maximize Returns with Cost-Efficient Dividend Investing

🧭 Portfolio on Cruise Control

Setting up DRIPs means your portfolio essentially runs on autopilot—automatically reinvesting dividends, reinvesting dividends, and quietly compounding returns without daily oversight. This feature is central to the benefits of DRIP investing, delivering passive income through DRIPs and automatic wealth building with minimal intervention.

Moreover, once you’re enrolled, your investment plan continuously purchases additional shares each dividend cycle, based solely on your existing holdings. Consequently, your portfolio stays steadily on course toward long-term growth.

Key advantages of a DRIP-powered cruise control portfolio:

📆 Automatic reinvestment after each dividend payout

🧠 Hands-off strategy removes emotional decision-making

💹 Fractional share purchasing maximizes reinvestment efficiency

🚫 No commissions or trade delays in most DRIP setups

📈 Compounding momentum builds with every cycle

Importantly, this disciplined automation encourages patience and long-term vision—letting your investments grow while you focus on living.

🪜 Compounding Wins Long-Term

True compounding isn’t magic—it’s mechanical. With DRIPs, when dividends are automatically reinvested, each payout buys more shares, those shares pay dividends, and the cycle continues—fueling compound growth with precision. This is the ultimate example of the benefits of DRIP investing, including passive income through DRIPs, automatic wealth building, and seamless reinvesting dividends.

Moreover, DRIPs thrive over time: in the early years, growth may seem modest, but as share quantity increases, dividends grow larger, accelerating returns significantly. Consequently, disciplined investors who remain enrolled often see exponential portfolio expansion. Importantly, the compounding effect becomes especially powerful after years or decades, as small re-investments snowball into substantial value.

💬 Q: Why does compounding work better with DRIPs?

A: Because every dividend you earn is instantly put back to work—buying more shares, creating a loop of automatic, scalable reinvestment that multiplies over time.

Stay the course, trust the math, and let time be your biggest asset.

📌 The Magic of Compound Interest: How to Double Your Money in 7 Years

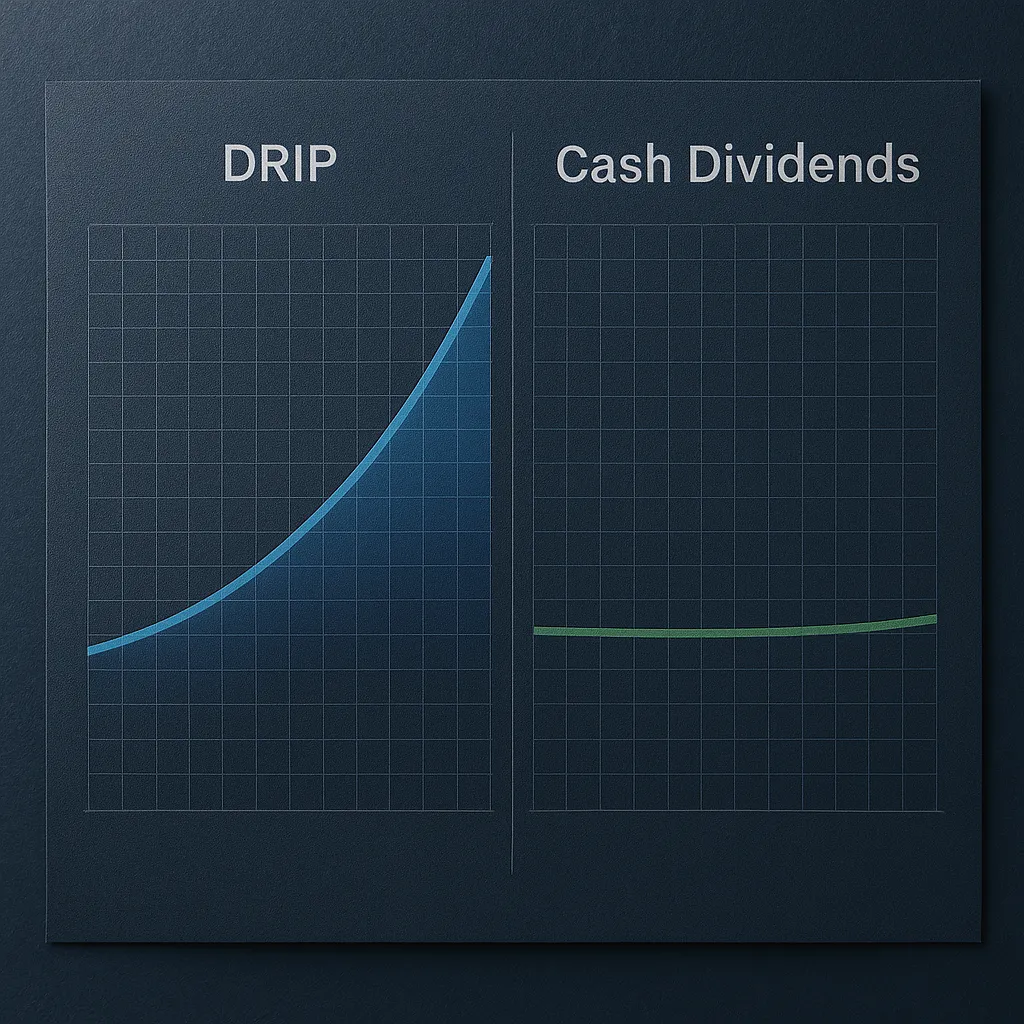

⚖️ DRIP vs. Cash Dividends: The Real ROI

💰 Should You Spend or Reinvest?

Deciding whether to take dividends as cash or opt for automatic reinvestment is a pivotal part of understanding the benefits of DRIP investing. By reinvesting, your dividends buy more shares—fueling passive income through DRIPs, automatic wealth building, and continuous reinvesting dividends. In contrast, spending dividends may meet short-term needs but often limits the potential for long-term portfolio growth.

Moreover, reinvested dividends compound over time—each cycle expands your share count, increasing future dividend payouts and accelerating wealth creation. Consequently, investors who stick with DRIPs often see stronger long-term performance than those who routinely cash out.

Importantly, the right choice depends on your financial stage, risk tolerance, and income needs.

| Strategy | Benefits | Drawbacks | Best For |

|---|---|---|---|

| Reinvest Dividends | Compound growth, long-term wealth building | No immediate cash access | Growth-focused, long-term investors |

| Spend Dividends | Cash flow, income for expenses | Slower growth, reduced compounding | Retirees or income-dependent investors |

📌 Reinvest Those Dividends—Differently: Smarter Strategies for Income Growth

📈 Real-World Comparison

Evaluating real DRIP outcomes helps illustrate the benefits of DRIP investing versus cash payouts. For example, an investor who began with $5,000 in dividend-paying stocks two decades ago and reinvested all dividends likely ended with significantly greater portfolio value—often 30–50% more than a non‑reinvestor. This demonstrates how passive income through DRIPs, automatic wealth building, and consistent reinvesting dividends can substantially amplify long-term results.

Moreover, account for tax efficiency: in many cases, reinvested dividends—while still taxable—are sheltered within retirement accounts, increasing net returns over time. Consequently, DRIP users who remain invested enjoy steadily compounding growth, even during volatile periods or economic downturns.

Most importantly, these real-world comparisons underscore that staying the course often outpaces timing the market or cashing out.

📌 4 Lessons Learned from 20 Years of Dividend Investing

📊 DRIP Tax Considerations

Understanding how dividends reinvested through DRIPs are taxed is essential to fully appreciate the benefits of DRIP investing. Even though dividends are automatically reinvested, the IRS treats them as taxable income in the year received—just as if you received cash. This reinforces key principles behind reinvesting dividends, passive income through DRIPs, and automatic wealth building.

Most dividends fall into two categories: qualified (taxed at capital gains rates) and ordinary (taxed as regular income). Every reinvestment becomes a new tax lot, complicating cost basis tracking.

Here’s how DRIP taxes vary by account type:

| Account Type | Tax Treatment | Notes |

|---|---|---|

| Taxable Brokerage Account | Dividends are taxable annually—even if reinvested | Requires tracking and 1099-DIV reporting |

| Roth IRA | No taxes on dividends or withdrawals if qualified | Best for long-term, tax-free compounding |

| Traditional IRA / 401(k) | No annual taxes; taxed as income upon withdrawal | Defers tax, enabling pre-tax compounding |

| DRIP with Discounted Shares | Taxed on full FMV of shares received | Discount must be included in total dividend income |

Moreover, retirement accounts simplify taxes and amplify DRIP growth potential. Consequently, many investors leverage DRIPs inside IRAs for optimal results.

📌 Understand DRIP tax implications and 1099-DIV requirements at SmartAsset

🛑 When to Opt Out of DRIPs

There are distinct scenarios when choosing to take dividends in cash rather than reinvesting them may better align with your financial needs—especially if you depend on that income. While the benefits of DRIP investing—such as automatic wealth building and passive income through DRIPs—are powerful for long-term growth, circumstances matter.

Consider opting out of DRIPs if:

💵 You rely on dividends for income, such as in retirement

🧾 You want to manage taxes proactively, avoiding phantom income

📊 You prefer to control when and how dividends are reinvested

🧠 You seek flexibility to redirect dividends to other assets or expenses

📉 You want to reduce exposure to a single company’s stock

Moreover, reinvested dividends can create taxable events without immediate cash benefits. Consequently, opting out can help maintain liquidity and strategic control—especially for income-focused investors.

📌 When to Reinvest Dividends—and When You Might Not Want To

🚀 Future-Forward: DRIPs in Your Wealth Strategy

🧓 Ideal for Retirement Accounts

DRIPs are especially well-suited for tax-advantaged retirement accounts, making them a powerhouse tool for both benefits of DRIP investing and automatic wealth building, particularly when aiming for passive income through DRIPs.

In accounts like Roth IRAs or Traditional IRAs, dividends reinvest without triggering annual tax liabilities. This allows reinvestment to proceed uninterrupted—free from the drag of capital gains taxes or Form 1099‑DIV complexities. Over time, this creates an ideal environment for reinvesting dividends and capturing maximum compound growth.

“DRIPs inside retirement accounts are like compounding on steroids—tax-free growth layered on top of disciplined reinvestment.”

Moreover, this setup simplifies long-term investing. No need to track multiple tax lots or worry about the timing of capital gains. Consequently, DRIPs in retirement accounts accelerate portfolio growth while reducing administrative headaches—ideal for investors with a long horizon and strategic patience.

📌 Bogleheads Forum: Community Discussion on DRIP Strategies and Investment Insights

💪 Pair DRIPs with Dollar-Cost Averaging

Combining DRIPs with dollar-cost averaging (DCA) creates a powerful investment rhythm—automatically reinvesting dividends while consistently adding new funds on a schedule. This synergy enhances both compound growth and strategic discipline, aligning with the benefits of DRIP investing, including automatic wealth building, passive income through DRIPs, and consistent reinvesting dividends.

Moreover, while DRIPs compound your dividends, DCA ensures fresh capital continues to flow, even in volatile markets. Consequently, your portfolio steadily expands—fueled by both reinvested income and regular contributions.

How DRIPs and DCA work together:

| Strategy | Primary Function | Key Benefit | Ideal Use Case |

|---|---|---|---|

| Dividend Reinvestment Plan (DRIP) | Reinvests dividends into more shares | Automates compounding | Long-term stockholders with dividend income |

| Dollar-Cost Averaging (DCA) | Invests fixed amounts on a schedule | Reduces timing risk | Investors making consistent monthly contributions |

📌 Dollar-Cost Averaging and DRIP Strategies: Interactive Brokers Webinar

🌪️ DRIPs in Volatile Markets

Investing in volatile markets can feel unnerving—but DRIPs offer a stabilizing force. By automatically reinvesting dividends, they help investors avoid trying to time markets or act on emotional impulses. This aligns powerfully with the benefits of DRIP investing, including passive income through DRIPs, automatic wealth building, and steady reinvesting dividends even during downturns.

Moreover, when stock prices dip, dividends reinvested via DRIPs buy more shares at lower entry points—enhancing your compound growth potential over time. Consequently, market swings often translate into an advantage rather than a setback. Importantly, this strategy fosters confidence and consistency—key traits for long-term investors who prioritize discipline over reacting to short-term noise.

📌 How Traders Can Take Advantage of Volatile Markets: Strategies for Smart Moves

🤖 Let Your Dividends Hustle for You

🧠 Recap: DRIPs Are for Strategic Investors

When it comes to building sustainable, long-term wealth, few tools are as effective and effortless as Dividend Reinvestment Plans. The benefits of DRIP investing—from automatic wealth building to passive income through DRIPs and consistent reinvesting dividends—cater to investors who value discipline over hype.

Here’s why DRIPs are a favorite among strategic investors:

🔁 They automate reinvestment, removing emotion from the equation

📉 They capitalize on market dips, buying more shares at lower prices

📈 They compound over time, increasing dividend income and equity

🛠️ They require no active management, yet deliver long-term results

🧠 They align with goal-driven, patient investing strategies

Moreover, DRIPs offer clarity in chaos—no timing, no noise, just consistent execution. Consequently, they’re an essential part of any long-range investment playbook.

📌 Explore how DRIP investing supports smart, long-term strategies at Seeking Alpha

⚙️ Automate and Win

Setting up DRIPs effectively turns your portfolio into a fully automated wealth engine. By automatically reinvesting dividends, DRIPs allow the power of compound growth to operate without daily intervention—reflecting the core benefits of DRIP investing, including automatic wealth building, passive income through DRIPs, and consistent reinvesting dividends.

Once activated, DRIPs take care of the rest. You don’t need to issue trading instructions or time the market—each dividend instantly adds to your share count, boosting future dividends in a seamless feedback loop. Moreover, because most plans are commission-free, there are no hidden costs eating into your returns. Consequently, every dividend dollar maximizes its long-term impact.

Table: Automation vs. Manual Investing: A Quick Comparison

| Feature | Automated (DRIP) | Manual Reinvestment |

|---|---|---|

| Dividend Use | Reinvested automatically | Requires manual reinvestment decisions |

| Timing | Immediate on payout date | May delay based on investor timing |

| Fees | Often commission-free | May incur trading or brokerage fees |

| Emotion Involvement | Low—set it and forget it | High—subject to market psychology |

| Long-Term Efficiency | High—optimized for compounding | Variable—depends on discipline and timing |

Importantly, automating your strategy removes friction—letting your portfolio perform while you focus on living.

📌 Manual Trading vs. Automated Trading: Which Strategy Is Right for You?

🛠️ How to Start DRIP Investing

Getting set up with a Dividend Reinvestment Plan (DRIP) is surprisingly straightforward. It’s an excellent way to unlock the benefits of DRIP investing, including automatic wealth building, passive income through DRIPs, and consistent reinvesting dividends—all without needing to watch the market daily.

Here’s your simplified roadmap:

Assess your brokerage or the company’s plan

Confirm whether your brokerage offers an in-house DRIP or check if the company sponsors its own direct plan. Either option supports passive income through DRIPs.Enroll in the plan

Enable DRIP reinvestment on qualified dividend-paying stocks. Many locations offer commission-free setups, maximizing every reinvested dollar.Maintain awareness but avoid micromanaging

Let the system work—dividends will automatically reinvest each payout date. This pull focus helps keep your investing consistent and emotional decisions at bay.Track cost basis and monitor performance over time

While participation is largely hands-off, you still may need to manage tax lots and 1099-DIV reporting for accurate portfolio records.

Important Note: Even though dividends are reinvested automatically, the IRS treats them as taxable income in the year earned. If you’re using a brokerage taxable account, track these events carefully.

📌 What Is DRIP Investing? A Beginner’s Guide to Growing Wealth Through Dividends

💬 Join the Conversation

Are you already using a DRIP? Thinking about starting one? Whether you’re stacking dividends, automating your growth strategy, or still weighing the pros and cons, your experience matters.

The benefits of DRIP investing—like automatic wealth building, passive income through DRIPs, and consistent reinvesting dividends—can look different depending on your stage of investing, your goals, and even your broker.

We’d love to hear from you:

What’s your favorite dividend-paying stock to DRIP?

Have you seen a noticeable difference in portfolio performance over time?

Do you prefer reinvesting or taking cash payouts—and why?

Moreover, your feedback helps new readers learn from real-world experiences. Consequently, whether you’re a DRIP veteran or just getting started, drop your thoughts in the comments below.

📌 Share your DRIP experience and learn from others on Reddit’s r/dividends community

🏁 Conclusion: DRIPs May Be Boring—But Boring Builds Empires

📊 In a world chasing quick wins, DRIPs offer lasting returns.

Flashy trends come and go, but the quiet power of reinvesting dividends keeps building—even when no one’s watching. In a landscape obsessed with short-term gains and speculative plays, DRIPs stand as a testament to automatic wealth building and financial patience.

The benefits of DRIP investing aren’t about overnight success—they’re about compounding, consistency, and letting time do the heavy lifting. Moreover, they offer a rare blend of strategy and simplicity: set it, forget it, and let your dividends hustle.

Consequently, investors who embrace DRIPs aren’t just playing the game—they’re setting the pace.

So choose slow. Choose steady. Choose strategy.

📌From budgeting to investing, the Investillect blog has you covered

📚 Top Books on DRIP Investing and Dividend Wealth Strategies

If you’re ready to take the next step in mastering the benefits of DRIP investing, these top-rated books are rich with insight, strategy, and long-term value:

📘 Investing in DRIPs by Alan Kerrman

A personal, practical guide for anyone ready to automate their investments and achieve financial freedom. Focuses on DRIPs and DSPPs with real-life application.

📗 Dividends Still Don’t Lie by Kelley Wright

The modern successor to Geraldine Weiss’s classic. This book leans into dividend yield patterns, blue-chip stocks, and long-term wealth preservation.

📙 The Ultimate Dividend Playbook by Josh Peters

Backed by Morningstar, this book dives into building, managing, and protecting a dividend-rich portfolio. Great for both beginners and seasoned investors.

📕 Get Rich with Dividends by Marc Lichtenfeld

A clear, step-by-step dividend strategy designed to deliver consistent returns—accessible, actionable, and time-tested.

🔍 Bonus Classics for Deeper Insight

Stocks for the Long Run by Jeremy Siegel — Historical context on compounding, inflation, and dividend power.

The Intelligent Investor by Benjamin Graham — The value investing bible; philosophy that aligns well with DRIP discipline.