Ever stared at your pay stub and winced at the healthcare deductions? You’re not alone. The average American spends over $5,000 annually on health insurance premiums alone—not counting the deductibles and copays that follow. That’s where understanding HSA vs FSA tax benefits can make a real financial difference.

But here’s what most people miss: there are legitimate ways to make those healthcare dollars work harder for you. Understanding health savings accounts, flexible spending accounts, and their tax benefits can literally put thousands back in your pocket.

I’ve spent 15 years helping people navigate health insurance options, and I’ve seen too many smart professionals leave money on the table simply because nobody explained how these accounts actually work.

The secret? It’s not just about picking a plan—it’s about strategically using tax-advantaged accounts alongside your coverage. And the difference between doing it right versus not bothering at all?

Health Savings Account (HSA) Explained: Benefits, Eligibility, and How It Works

Health Savings Account (HSA) Explained: Benefits, Eligibility, and How It Works

Understanding Health Savings Accounts (HSAs)

What is an HSA and who qualifies

When comparing HSA vs FSA tax benefits, it’s clear that Health Savings Accounts (HSAs) stand out as versatile, tax-favored tools for managing medical expenses. However, eligibility hinges on a few key requirements: you must be covered by an IRS-approved high-deductible health plan (HDHP), have no conflicting coverage, and not be claimed as a dependent on someone else’s tax return.

Moreover, whether you’re self-employed, running a household, or navigating healthcare solo, meeting these criteria grants access. That said, once you enroll in Medicare, contributions to these healthcare savings accounts must stop—so strategic timing is crucial.

What Is a Health Savings Account (HSA)? Tax Benefits, Rules, and Uses

Contribution limits and deadlines

HSA contribution limits are set annually by the IRS, and for 2025 those limits are $4,300 for individuals and $8,550 for family coverage—with an additional $1,000 catch‑up allowed if you’re age 55 or older (“HSA contribution limits,” 2025). These annual maximums include contributions from both you and your employer. After turning 55, you’re entitled to the extra “catch‑up contribution” whether you’re self-employed or employed.

Importantly, you have until the federal tax filing deadline—typically April 15—to make contributions to your account for the previous tax year. For example, funds deposited between January 1 and April 15, 2025, can be applied to either the 2024 or 2025 contribution limit, depending on your designation.

Deadlines at a Glance:

2025 individual limit: $4,300 (+$1,000 catch‑up if 55+)

2025 family limit: $8,550 (+$1,000 catch‑up)

Contribution window: Jan 1–Dec 31 for the current year; Jan 1–Apr 15 for prior year

Maximizing your HSA contributions before these deadlines is one of the most effective strategies to boost HSA tax benefits and grow your health savings account balance.

HSA Contribution Limits: How Much You Can Save Tax-Free Each Year

Triple tax advantages explained

Health Savings Accounts (HSAs) come with a unique financial edge: a triple tax advantage that few other accounts can match. First, contributions to your HSA are tax-deductible, meaning every dollar you stash away lowers your taxable income. Second, any interest, dividends, or investment gains inside the account grow completely tax-free. Third, when you use those funds for qualified medical expenses—from prescriptions to dental care—you won’t owe a cent in taxes on withdrawals.

When comparing HSA vs FSA tax benefits, Health Savings Accounts (HSAs) offer unmatched flexibility and tax advantages. To qualify, you need a high-deductible health plan, no disqualifying coverage, and you can’t be a dependent. Plus, payroll deductions can be FICA-exempt, boosting your savings. Once enrolled in Medicare, contributions must stop. Unlike FSAs, HSAs allow funds to roll over, grow tax-free, and be invested. Many treat them as stealth retirement accounts—saving now, reimbursing later. This makes healthcare savings accounts a smart move for both immediate medical costs and long-term financial growth.

| Tax Benefit | What It Means |

|---|---|

| Tax-deductible contributions | Reduces your taxable income for the year |

| Tax-free investment growth | Earnings from interest or investing aren’t taxed |

| Tax-free withdrawals | No tax on withdrawals used for qualified medical expenses |

| FICA exemption (via payroll) | Potential savings on Social Security and Medicare taxes |

Using an HSA for Retirement: Unlock Tax Advantages and Boost Long-Term Savings

Investment options to grow your HSA funds

When weighing HSA vs FSA tax benefits, one major advantage of a Health Savings Account (HSA) is its investment potential. Once your HSA balance exceeds your provider’s cash threshold—typically $1,000 to $2,000—you can invest the excess, much like in a 401(k) or IRA. In fact, this turns your HSA into a healthcare investment account, allowing your funds to grow tax-free over time. Common investment options include:

Index Funds – Low-fee, diversified, and ideal for long-term growth

ETFs – Flexible, tax-efficient, and easy to rebalance

Mutual Funds – Actively managed options for varied risk tolerance

Target-Date Funds – Hands-off investing aligned with your retirement timeline

“An HSA isn’t just a savings account—it’s a silent wealth builder when you invest it wisely.”

Pro tip: Reinvest gains and delay reimbursements to maximize your HSA’s compounding power.

Long-Term Benefits of Investing Your HSA: Grow Tax-Free Wealth for Retirement

Flexible Spending Accounts (FSAs) Demystified

FSA eligibility requirements

In the HSA vs FSA tax benefits debate, Flexible Spending Accounts (FSAs) offer upfront savings but come with stricter rules. These pre-tax spending accounts are employer-sponsored and designed to cover healthcare, vision, or dependent care expenses. To qualify, you must work for a company that offers an FSA and be eligible for its group medical plan—even if you don’t enroll.

Moreover, contributions—capped annually by the IRS—can come from you, your employer, or both. FSAs typically cover you, your spouse, and eligible dependents. However, funds are “use-it-or-lose-it,” unless your employer allows a grace period or limited carryover.

Here’s an easy reference table:

| FSA Eligibility Feature | Requirement Details |

|---|---|

| Employer-offered plan | Must be provided by your workplace and open during enrollment |

| Group medical plan eligibility | You must qualify, even if not enrolled |

| Covered individuals | You, spouse, and IRS-defined dependents |

| Fund availability | Full annual contribution accessible from Day 1 of plan year |

| Rollover policy | Dependent on employer: grace period or limited carryover allowed |

What Is a Flexible Spending Account (FSA)? Benefits, Limits, and How It Works

Annual contribution limits

When evaluating HSA vs FSA tax benefits, it’s crucial to understand annual contribution limits. Each year, the IRS adjusts the cap for these tax-advantaged accounts. For 2025, you can contribute up to $3,300 pre-tax to a Medical FSA—a slight bump from 2024’s $3,200.

Additionally, many employer plans offer a carryover feature, allowing up to $660 to roll into the next year, depending on your plan’s grace period rules. Meanwhile, if you opt for a Dependent Care FSA, limits remain unchanged at $5,000 per household or $2,500 if married filing separately.

Below is a snapshot of the key limits:

| FSA Type | 2025 Contribution Limit | Max Carryover |

|---|---|---|

| Medical FSA | $3,300 | $660 |

| Dependent Care FSA | $5,000 / $2,500* | N/A |

* $5,000 if single or married filing jointly; $2,500 if married filing separately. Contributions reduce taxable income, helping maximize tax savings on healthcare spending.

2025 FSA Contribution Limit: Employees Can Contribute Up to $3,300 – Annual Election Required

The “use it or lose it” rule and grace periods

In the HSA vs FSA tax benefits comparison, Flexible Spending Accounts (FSAs) come with one notorious catch: the “use-it-or-lose-it” rule. If you don’t spend your FSA funds by the plan year’s deadline, you risk forfeiting them.

Fortunately, many employers add safeguards to soften the blow. Some offer a grace period—an extra 2.5 months to use leftover funds. Others allow a carryover, typically up to $660 into the next year.

However, plans can offer one or the other—not both. That’s why it’s essential to review your plan during open enrollment and monitor expenses to protect your tax-saving account from waste.

The IRS “Use-It-or-Lose-It” Rule: What It Means for Your FSA Funds

Qualifying medical expenses

Flex your FSA tax benefits—and make the most of HSA vs FSA tax benefits—by using your funds on a wide range of eligible healthcare costs. These tax-advantaged healthcare accounts let you cover both everyday needs and surprise medical expenses with pre-tax dollars.

From prescriptions and copays to dental work and mental health services, you can use these accounts strategically to ease your out-of-pocket burden while maximizing your tax savings.

Common qualifying expenses include:

Doctor and specialist visits

Prescription medications

Dental treatments (cleanings, fillings, extractions)

Eyeglasses, contact lenses, and vision exams

Over-the-counter medications and supplies (e.g., pain relievers, first-aid kits)

Mental health counseling and therapy

Medical equipment like crutches or blood pressure monitors

Travel costs related to medical care (HSA only)

What doesn’t qualify: cosmetic procedures, general wellness supplements, or gym memberships—unless medically prescribed. Always check with your plan administrator and consult IRS guidelines to ensure eligibility and avoid penalties.

IRS Publication 502: Medical and Dental Expenses – What’s Tax-Deductible

Dependent care FSA options

A Dependent Care FSA (DCFSA) offers a smart, tax-advantaged way to manage care costs while you work—further highlighting the value in HSA vs FSA tax benefits. Contributions are deducted straight from your paycheck, lowering your taxable income and boosting your overall FSA tax benefits.

Eligible expenses include daycare, preschool, summer day camps (excluding overnight), before- and after-school programs, work-related babysitting, and even adult daycare for disabled dependents. These pre-tax care accounts are especially valuable for working parents and caregivers aiming to ease the financial load without sacrificing tax efficiency.

| Feature | Details |

|---|---|

| 2025 Contribution Limit | $5,000 per household / $2,500 if married filing separately |

| Eligible Dependents | Children under 13, disabled spouses, older parents who rely on you |

| Covered Expenses | Daycare, preschool, day camps, adult daycare, work-related babysitting |

| Fund Access | Available only as contributions are made |

| Use-It-or-Lose-It Rule | Applies—no rollover or grace period unless specified by employer |

DCFSA funds can’t be used for tutoring, overnight camps, or non-dependent care. Planning ahead ensures you capture maximum pre-tax dependent care savings.

IRS Publication 503: Child and Dependent Care Expenses – Tax Rules and Eligibility

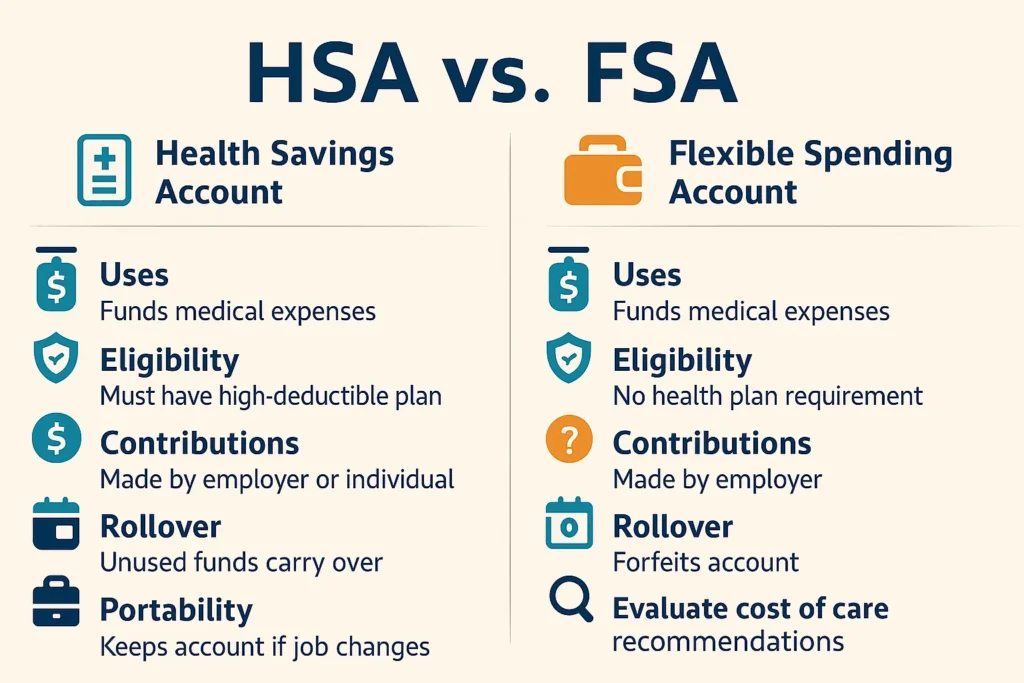

Comparing HSAs and FSAs

Key differences in eligibility criteria

While both HSAs and FSAs deliver powerful tax-advantaged savings, their eligibility requirements are worlds apart—making HSA vs FSA tax benefits a key comparison for smart financial planning.

To qualify for an HSA, you must have a high-deductible health plan (HDHP), not be enrolled in Medicare, and can’t be claimed as someone else’s dependent. HSAs are available to individuals, families, and even the self-employed. Plus, the account is yours—it’s portable and not tied to your employer.

On the other hand, FSAs are strictly employer-sponsored. You can’t open one independently, though you only need to be eligible for your employer’s group health plan—not necessarily enrolled. FSAs also come with use-it-or-lose-it restrictions, and the employer holds control of the account.

“HSAs give you autonomy; FSAs tie you to your employer’s rules. Knowing the difference could save—or cost—you hundreds.”

These distinct requirements make it crucial to match the right account to your financial and medical situation.

HSA vs. FSA: Key Differences, Benefits, and Which One’s Right for You

Portability between employers

When it comes to job changes, HSA vs FSA tax benefits highlight a crucial difference: portability. HSAs are fully portable—your account goes with you whether you change jobs, retire, or go freelance.

Since you own the account, you can continue contributing (if eligible), investing, and using the funds on qualified expenses. This makes HSAs not just tax-efficient, but also one of the most portable healthcare savings accounts available—unlike FSAs, which typically end with your job.

FSAs, however, are tied to your employer. Once you leave a job, you typically forfeit access to unused FSA funds unless you qualify for COBRA continuation—which often isn’t cost-effective. FSAs don’t follow you to a new employer, and any new FSA must be set up under your next job’s plan.

“Your HSA follows you like a shadow—your FSA disappears when you walk away.”

This key difference in portability makes HSAs a stronger long-term financial asset, especially for those with changing career paths.

IRS Publication 969: Health Savings Accounts and Other Tax-Favored Health Plans

Rollover capabilities

One of the biggest distinctions in the HSA vs FSA tax benefits conversation comes down to rollover rules. Here’s how they stack up:

HSA funds roll over automatically year after year, with no expiration. There’s no limit to how much you can carry forward.

FSA funds are more limited. Most plans follow a “use-it-or-lose-it” policy unless your employer offers a grace period or limited carryover.

Employers can choose either a 2.5-month grace period or a carryover of up to $660—but not both.

These differences impact how you plan and save for healthcare expenses annually.

| Feature | HSA | FSA |

|---|---|---|

| Year-to-year rollover | Yes – unlimited, automatic | Sometimes – limited, employer-dependent |

| Grace period | Not applicable | Up to 2.5 months (if offered) |

| Carryover allowance | Unlimited | Up to $660 (2025), if employer allows |

| Ownership | Account holder owns the funds | Employer controls access and policies |

Does Your FSA Roll Over? What to Know About Carryovers and Deadlines

Which account suits different life situations

Choosing between an HSA and FSA comes down to your healthcare needs, financial goals, and life stage. Understanding the HSA vs FSA tax benefits can unlock serious savings through these tax-smart healthcare accounts.

For young professionals, an HSA paired with a high-deductible plan offers long-term perks—tax-free growth, investment potential, and no pressure to spend right away. In contrast, growing families often prefer FSAs for predictable costs like pediatric visits or braces.

If you’re self-employed, HSAs are your only option. Nearing retirement? HSAs help you stack tax-free funds for future care. And for dual-income parents, a Dependent Care FSA is a smart move to offset childcare costs.

Q: Can I have both an HSA and an FSA?

A: Yes, but only if the FSA is limited-purpose—covering dental and vision only—so it doesn’t disqualify your HSA eligibility.

HSA vs. FSA: Which Health Account Saves You More Money?

Maximizing Tax Benefits

How HSAs and FSAs reduce your taxable income

Both HSAs and FSAs offer a powerful way to cut your tax bill by using pre-tax dollars for eligible expenses. Contributions to either account are deducted from your gross income, reducing your taxable base and boosting your overall savings.

Here’s how each one helps lower your tax burden:

HSA contributions reduce your adjusted gross income (AGI), helping you qualify for additional tax credits or deductions.

HSA payroll contributions may also avoid FICA taxes, adding even more value to your savings strategy.

HSA balances grow tax-free, and you pay no taxes on withdrawals used for qualified medical expenses.

FSA contributions are withheld pre-tax, lowering the income you report to the IRS.

FSAs immediately lower your taxable income, especially useful for covering routine healthcare and childcare expenses.

Neither account requires itemizing deductions to benefit—you save straight from your paycheck.

How FSAs Save You Money on Taxes: A Smart Guide to Pre-Tax Health Spending

Strategies for combining with other tax deductions

Maximizing HSA vs FSA tax benefits means thinking beyond healthcare. When used strategically, these tax-efficient savings strategies can significantly boost your overall financial picture.

Pairing an HSA with an IRA, for example, allows you to reduce taxable income through both healthcare and retirement contributions. Since HSA contributions lower your adjusted gross income (AGI), you might even unlock additional credits—like the Earned Income Tax Credit or student loan interest deductions.

Furthermore, if your medical costs exceed HSA or FSA limits, unreimbursed expenses above 7.5% of your AGI can be itemized. Families can also stack a Dependent Care FSA with the Child and Dependent Care Credit. And after 65, HSA funds can be used penalty-free for non-medical expenses—just taxed like a traditional IRA.

“Combining your HSA with other deductions isn’t just smart—it’s a tax strategy that can save you thousands.”

How to Combine an HSA with Other Retirement Accounts for Maximum Tax Efficiency

Record-keeping requirements for tax purposes

To fully leverage HSA vs FSA tax benefits, meticulous recordkeeping is a must. These tax-favored healthcare accounts require proof that your spending meets IRS guidelines.

Be sure to keep receipts, invoices, and Explanation of Benefits (EOBs) that clearly document each qualified medical expense. Not only does this help during tax season, but it also protects you in case of an audit—ensuring your savings don’t turn into unexpected liabilities.

| Requirement | HSA | FSA |

|---|---|---|

| Documentation needed | Keep receipts and records for all qualified expenses | Submit receipts for claims; employer may require upfront substantiation |

| When to keep records | Indefinitely, or until IRS audit period ends | Until claims are processed and reimbursement received |

| Submission to administrator | Only if IRS requests proof | Usually required before reimbursement |

| Expense tracking | Track date, amount, and type of qualified expense | Track for each claim within plan deadlines |

| Audit risk | IRS may request proof of qualified withdrawals | Employer may audit claims for eligibility |

Good record-keeping not only protects your tax savings but also helps you confidently navigate tax filing season.

HSA Requirements: What to Know About Receipts and Recordkeeping

Strategic Planning for Healthcare Costs

Creating a healthcare budget with tax-advantaged accounts

Building a smart healthcare budget starts with understanding how HSAs and FSAs can stretch your dollars further. Follow these steps to optimize your spending:

Estimate your annual medical costs, including premiums, prescriptions, co-pays, dental, vision, and unexpected emergencies.

Use your HSA with a high-deductible health plan to cover immediate expenses and grow savings long term.

Maximize your HSA contributions to benefit from triple tax advantages—tax-deductible deposits, tax-free growth, and tax-free withdrawals.

Allocate your FSA funds carefully for predictable yearly expenses due to the use-it-or-lose-it rule.

Regularly track and review your actual medical spending to adjust your contributions and avoid forfeiting unused FSA funds.

Taking these steps helps you capture every tax benefit while managing healthcare costs efficiently.

The Ultimate Guide to HSA & FSA Eligible Expenses and Smart Savings Strategies

Timing medical expenses for maximum tax benefits

Strategic timing is key to maximizing HSA vs FSA tax benefits. These tax-optimized healthcare accounts reward proactive planning—especially when it comes to expenses and contributions.

With FSAs, the use-it-or-lose-it rule means you should schedule healthcare purchases—like elective procedures or prescription eye-wear—within the plan year or grace period to avoid forfeiting funds.

In contrast, HSAs offer long-term flexibility. Funds roll over and can be invested, allowing you to delay reimbursement and let your account grow tax-free. Plus, you can contribute up until the IRS deadline (usually April 15) for the prior year, giving you more time to align contributions with your tax strategy.

| Timing Strategy | HSA | FSA |

|---|---|---|

| Expense planning | Pay now or delay reimbursement indefinitely | Spend within plan year or grace period |

| Fund rollover | Unlimited rollover year after year | No rollover unless employer offers carryover/grace period |

| Contribution deadline | Until tax filing deadline (typically April 15) | Set by employer, usually within plan year |

| Investment growth potential | Tax-free, if funds remain invested | No investment option |

Maximize Your FSA or HSA: Year-End Tips and 2025 Planning Strategies

Family planning considerations

When planning for a growing family, understanding HSA vs FSA tax benefits is key to managing healthcare costs wisely. These family-focused tax savings accounts can ease financial strain while delivering meaningful tax breaks.

HSAs, when paired with a high-deductible plan, offer flexibility to save and invest for both immediate and future medical needs—like prenatal care, delivery, and pediatric visits. Meanwhile, FSAs shine for budgeting annual expenses, including co-pays, prescriptions, and daycare via a Dependent Care FSA.

However, due to the FSA “use-it-or-lose-it” rule, estimating expenses is critical. Plan ahead, align contributions with your timeline, and maximize every tax-saving opportunity.

10 Smart Ways to Use Your HSA or FSA for Family Planning Expenses

Using HSAs as retirement savings vehicles

In the HSA vs FSA tax benefits landscape, Health Savings Accounts (HSAs) stand out as powerful long-term healthcare savings vehicles—especially for retirement planning.

Unlike FSAs, HSAs offer a rare triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. As a result, HSAs can double as supplemental retirement accounts, giving you a flexible, tax-efficient way to cover future healthcare costs—or even non-medical expenses after age 65, taxed like a traditional IRA.

Consider these eye-opening stats:

Over 70% of retirees face significant healthcare costs in retirement. HSAs allow you to invest and potentially grow your balance tax-free for decades. After age 65, withdrawals for non-medical expenses are allowed penalty-free (though taxed as income), providing retirement spending flexibility.

Over 70% of retirees face significant healthcare costs in retirement. HSAs allow you to invest and potentially grow your balance tax-free for decades. After age 65, withdrawals for non-medical expenses are allowed penalty-free (though taxed as income), providing retirement spending flexibility.

Unlike FSAs, HSAs let funds roll over indefinitely. You can invest in stocks, bonds, or mutual funds, potentially supercharging your savings over time. Using your HSA as a long-term savings vehicle helps prepare for rising healthcare expenses with unmatched tax perks.

How HSAs Can Boost Your Retirement Strategy: Tax Benefits and Long-Term Growth

FAQ: Top Questions on HSA vs FSA Tax Benefits

HSAs offer triple tax advantages: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. FSAs also reduce taxable income but have no tax-free growth and funds usually expire yearly.

HSAs require enrollment in a high-deductible health plan and no Medicare coverage. FSAs are employer-sponsored, so eligibility depends on your employer’s plan.

Flexible Spending Accounts (FSAs) and Job-Based Health Coverage

You can contribute to both only if the FSA is a limited-purpose FSA covering dental and vision expenses; otherwise, contributing to both is generally not allowed.

Can You Contribute to Both an HSA and an FSA in the Same Year?

HSAs have higher contribution limits, which vary yearly and depend on whether coverage is individual or family. FSAs have lower limits and do not differentiate by coverage type.

HSA & FSA Contribution Limits: Stay Updated to Optimize Your Health Benefits

HSA funds roll over indefinitely without penalty. FSA funds generally expire at year-end unless your employer offers a grace period or carryover option.

HSA contributions made through payroll deductions are exempt from federal income tax and often from payroll taxes like Social Security and Medicare.

Maximize Tax Benefits with a Health Savings Account (HSA): Key Considerations

Yes, many HSAs allow you to invest your funds in mutual funds, stocks, and bonds, similar to retirement accounts, growing your balance tax-free over time.

How HSAs Can Strengthen Your Retirement Plan: Tax-Free Growth & Smart Withdrawals

Withdrawals from HSAs for qualified expenses are tax-free with no deadlines, while FSAs require expenses to occur within the plan year or grace period to avoid forfeiture.

HSA vs. FSA: Compare Benefits, Eligibility, and Which One’s Right for You

Wrapping It Up

Smart Health, Smarter Money: Mastering HSAs and FSAs for Financial Wellness

Navigating the world of health insurance and tax-advantaged accounts doesn’t have to be overwhelming. By understanding the key differences between HSAs and FSAs, you can make informed decisions that align with your healthcare needs and financial goals. Remember that HSAs offer long-term investment potential with triple tax advantages, while FSAs provide immediate tax savings with simpler qualification requirements.

Take time to evaluate your healthcare spending patterns and tax situation to determine which account—or combination of accounts—works best for you. Whether you’re looking to reduce your taxable income, prepare for future medical expenses, or strategically plan for healthcare costs in retirement, these financial tools can help you take control of your healthcare spending while keeping more money in your pocket. Start maximizing these benefits today to secure your financial and physical well-being for years to come.

HSA or FSA? Visit Investillect.com to find out which saves you more.

Other Resources and Tools to Level Up Your Health Finance Game

If you’re ready to dive deeper or want help managing your healthcare dollars like a pro, these tools and resources can guide the way:

Calculators & Planners

Calculators & Planners

HSA/FSA Contribution Calculators – Use tools from providers like Fidelity or SmartAsset to estimate tax savings and plan your annual contributions.

Healthcare Expense Estimators – Check out tools from Healthcare.gov or your insurance provider to forecast medical costs and align your account funding.

Educational Guides

Educational Guides

IRS Publications 969 & 502 – These explain qualified medical expenses, contribution limits, and tax details straight from the source.

Kaiser Family Foundation (KFF) Reports – Get sharp insights into healthcare trends, employer contributions, and average out-of-pocket costs.

Books Worth Reading

Books Worth Reading

The Healthcare Labyrinth by Marc S. Ryan – A no-nonsense guide to decoding America’s health insurance system and maximizing your benefits.

Get What’s Yours for Medicare by Philip Moeller – A savvy resource for navigating Medicare, with insight that also applies to HSAs in retirement planning.

Smart Health Choices by Les Irwig, Judy Irwig, et Al – Though geared toward medical decision-making, it sharpens your ability to evaluate healthcare options with financial consequences in mind.

Smart Apps & Account Platforms

Smart Apps & Account Platforms

Lively, Fidelity, and Optum Bank – These HSA/FSA platforms offer user-friendly dashboards, mobile apps, and educational content.

Monarch Money & YNAB – Personal finance apps that let you track healthcare spending alongside your broader budget.

Talk to the Pros

Talk to the Pros

Financial Advisors with Healthcare Expertise – A certified financial planner (CFP) or tax advisor can tailor a strategy to your income, coverage, and retirement goals.

Leveling up your healthcare strategy takes more than guesswork—it takes the right tools, some smart reads, and a clear view of your financial future.