🚨 Picture this: your car starts making that “I’m-about-to-break” noise, your dog swallows a sock (again), or your boss casually mentions “restructuring.” Now what? If your current plan involves crossing your fingers and whispering sweet nothings to your credit card, it’s time to talk about emergency funds—your financial superhero in sweatpants, otherwise known as a rainy day fund.

The truth? Life throws curve-balls faster than a toddler with a juice box. That’s why having an emergency fund isn’t just smart—it’s essential. But don’t worry, we’re not talking about stashing away Fort Knox. Even a small buffer can save you from big-time stress (and those awkward “Can I borrow…” texts 😬).

In this guide, you’ll discover exactly how much cash cushion you need, where to park it so it’s safe but still within arm’s reach, and how to get started—without surviving on instant noodles.

Plus, we’ll clear up common myths (no, your credit card isn’t a backup plan) and share real-life tips to build your buffer without pain.

📌 Oh, and according to CBS, 57% of Americans can’t cover a $1,000 emergency. Let’s fix that—before your water heater explodes. 💥

Why Emergency Funds Matter

What It’s For 💡

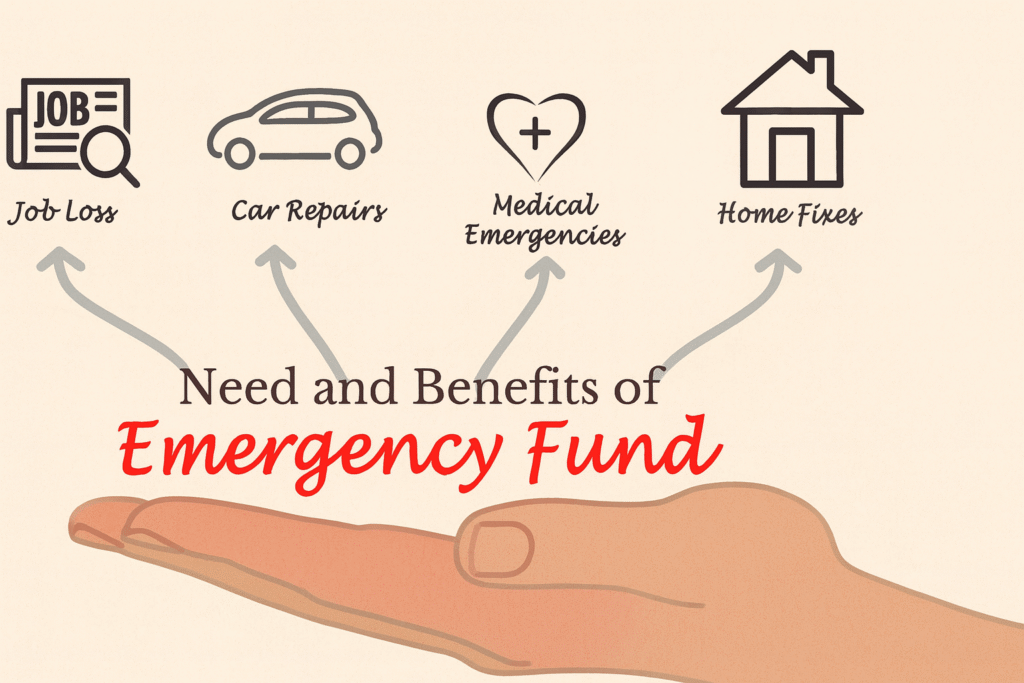

Let’s get one thing straight: emergency funds aren’t just a “nice-to-have”—they’re your financial buffer between life’s chaos and your bank account’s dignity. First, imagine losing your job 😬. Then, imagine doing it without a stash of cash to keep you afloat. Now imagine trying to stay calm while also explaining to your landlord that “vibes” will cover the rent this month.

Whether it’s a sudden layoff, a surprise medical bill, or your car deciding it’s done with adulting 🚗💥, emergency funds are built to absorb the hit. And no, using your credit card as a flotation device doesn’t count—unless you like debt spirals and interest rates that bite harder than a raccoon🦝 in a trash can.

Moreover, by having a ready stash, you dodge the “I guess I’ll just open another credit card” panic spiral. And trust us, nothing kills your credit score faster than a dozen late-night finance decisions and a shaky payment plan.

So, before disaster strikes, give your future self the gift of chill. Because when life gets messy, your emergency fund should be the calm in the financial storm. ⛅💵

📌 Checkout CFPB’s Emergency Fund Guide

Don’t Swipe Your Safety Net

Let’s clear this up right now: your credit card is not an emergency fund. Sure, it might feel like a lifeline when your water heater explodes or your cat swallows something sparkly—but relying on plastic during a crisis is like using a pool floaty in a hurricane. 🌪️

Yes, credit cards are convenient. However, that convenience comes with sky-high interest rates, sneaky fees, and the looming specter of debt. And let’s be real—stress-eating ramen noodles while dodging collection calls isn’t exactly a financial strategy. 😬

That’s why a crisis cushion—a.k.a. your emergency fund—exists. It’s cash you actually own, not money you’re borrowing from Future You (who, by the way, already has enough on her plate).

Moreover, using an emergency fund means you handle the emergency and move on—no monthly minimums haunting you later. So instead of trusting a high-interest safety net, build your own with cash that cushions, not crushes.

📌 Why Emergency Funds Beat Credit Cards Every Time →

Spoiler alert: Your future self will thank you—and so will your credit score. 💁♀️📈

How Much to Save in Emergency Funds

Finding Your Just-in-Case Number

Ah yes, the magical 3–6 months rule—sounds like advice from a financial fairy godmother, right? But before you wave it off as vague finance speak, let’s break it down and make it real.

Spoiler: your emergency funds aren’t about guessing—they’re about your actual life.

Start by tallying your essential monthly costs: rent or mortgage, groceries (no, not just snacks), utilities, insurance, and anything else you need to stay upright. Multiply that by 3 for a mini buffer, or 6 if you like sleeping peacefully at night. 🛏️✨

For example, if your essentials total $2,000/month, your oh-no fund goal is $6,000–$12,000. But—and this is key—you don’t have to get there overnight. Even $500 is better than $0. Think of it like building a lasagna: layer by layer, deliciously protective.

Also, this isn’t a one-size-fits-all deal. Got a stable job with great benefits? Maybe 3 months is fine. Freelance in the gig jungle? You’ll want more cushion than a beanbag chair.

So yes, the 3–6 months rule matters—but personalize it. Because emergencies don’t care about averages—they care about you.

🧠 Need help calculating? We’ve got a simple tool right here.

Turn Side Hustles into Safety Nets 🛍️➡️💵

You don’t have to cut out all joy (or coffee) to build your emergency funds—just tap into the magic of your side hustle. Whether it’s pet sitting, DoorDashing, freelancing, or flipping vintage mugs on eBay, that extra cash has superhero potential 🦸♀️💰.

Instead of letting side gig money vanish into everyday spending, route it straight into your safety stash. Treat it like it doesn’t exist (unless life hits the fan), and watch your uh-oh account grow faster than your friend’s houseplant collection. 🌿📈

Pro tip: Open a separate high-yield savings account just for your side-hustle earnings. That way, you won’t accidentally spend it on late-night online cart splurges. You know the ones.

This strategy builds your financial buffer without sacrificing your main paycheck—or your daily comforts. Plus, when you link effort directly to progress, saving feels earned and even a little satisfying.

📌 Need inspiration? Check out Coursera’s Guide to Side Hustles and How to Get Started and start stacking your stress-free stash.

Make Saving a Game (Yes, Really) 🎯📈

Saving doesn’t have to feel like punishment. In fact, turning it into a game might be the secret to sticking with it—and actually enjoying the process. Yes, we said fun and emergency funds in the same sentence. 😎🎉

Start with low-stakes challenges: try a “no-spend week,” stash every $5 bill you get, or save a dollar every day for 30 days. You can even set “boss level” goals like saving $100 every time your favorite sports team loses (pain into progress, baby). 🏈💸

Apps like Qapital, YNAB, or even your phone’s reminders can gamify the process, track your streaks, and cheer you on. You’ll feel like you’re leveling up—financially.

And don’t forget rewards! Celebrate milestones (like hitting your first $500) with a treat that doesn’t undo your progress. Maybe a fancy coffee or a smug selfie with your growing balance. ☕📸

Bottom line? Gamifying savings makes it less about sacrifice and more about success. And suddenly, building emergency funds feels less like a chore—and more like a flex.

📌 Want a printable challenge tracker? Download the fun, free savings challenge printables → and let the saving games begin!

Smart Habits That Grow Emergency Funds

Turn Windfalls Into an Oops-Proof Fund 🎉💵

Let’s talk about the most exciting kind of money: the unexpected kind. Tax refunds, work bonuses, birthday cash from grandma—you didn’t plan for it, but suddenly it’s there, shining like financial fairy dust. ✨ Now before it morphs into a new gadget or 17 takeout orders, consider this: funnel it into your emergency funds.

Why? Because these one-time boosts are perfect for padding your oops-proof fund. You won’t miss the money—after all, it wasn’t part of your regular budget—and it gives your savings a serious glow-up. 💫

Let’s say your tax refund is $1,200. Instead of blowing it on things you’ll forget by next Tuesday, send $800 to your emergency stash, treat yourself to a nice dinner, and save the rest for guilt-free fun. Balance, baby. 🥂💡

Bonuses? Same deal. Before you go full Beyoncé at Target, split it: some to your emergency fund, some to debt, and a little to joy. This method builds savings without the pain of cutting back.

📌 Scored a bonus or unexpected cash? Check out these smart windfall strategies and make every dollar count. Because future-you deserves more than impulse buys. 🎯💼

Emergency fund: 1. Impulse buys: 0. 🛑💳

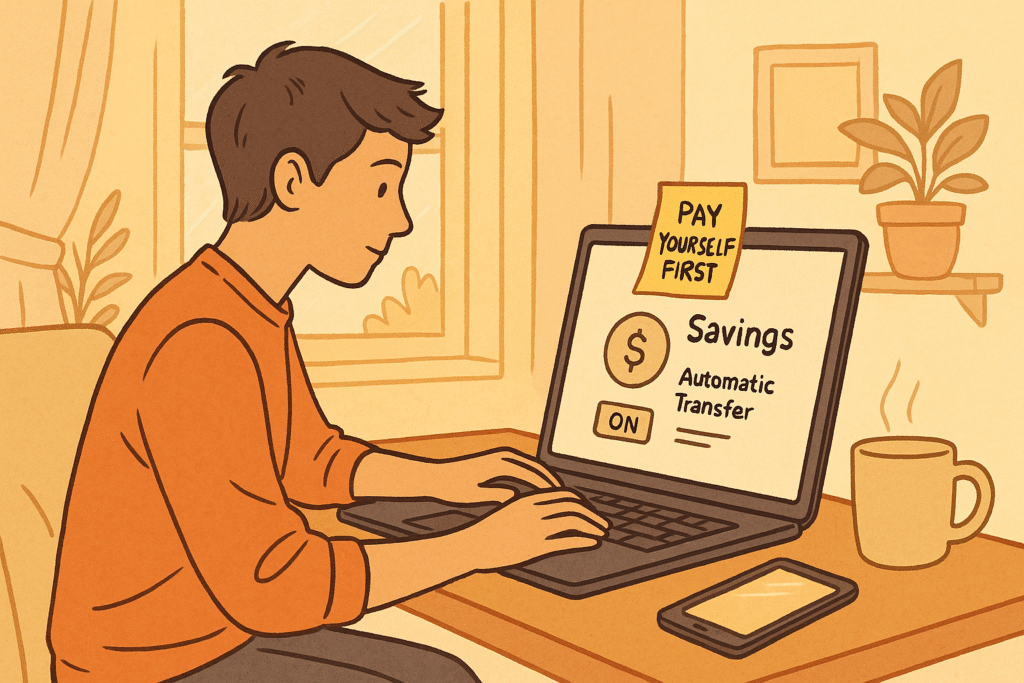

Outsmart Lifestyle Creep (Before It Sneaks Up) 🧟♀️💸

Ah, lifestyle creep—the sneakiest budget villain of them all. One minute you get a raise, the next you’re suddenly paying for five streaming services, $9 lattes, and a dog spa membership your dog didn’t ask for. 🐶🫧

But here’s the thing: just because your income grows doesn’t mean your spending should balloon alongside it. Instead, use that new money to beef up your emergency funds—a.k.a. your future-proof fund. Because peace of mind > premium gym you never go to. 🏋️♂️💤

Here’s the play: when your paycheck gets a bump, pause before upgrading your life. Automate a chunk of that raise straight into savings. That way, your lifestyle doesn’t notice, but your emergency fund throws a party. 🎉

Even better? You can still enjoy small upgrades (like actual guac at Chipotle 🥑), while also knowing that your financial foundation isn’t cracking beneath your feet.

📌 Want help dodging financial bloat? Check out our Lifestyle Creep Checklist to stay grounded—and growing.

Remember, the goal isn’t to look rich. It’s to be ready when life goes sideways. And trust us—your future self doesn’t want to cancel Hulu in a crisis. 😅📉

What to Do Once It’s Fully Funded