When it comes to building long-term wealth, few tools offer the flexibility and tax advantages of a Roth IRA. So, what is a Roth IRA, exactly? It’s a powerful retirement savings account that allows your money to grow tax-free. Even better, unlike traditional IRAs, qualified withdrawals during retirement are completely tax-exempt.

To put it simply, understanding how Roth IRAs work can give you a serious edge in financial planning. Whether you’re just starting out or already investing, this Roth IRA guide lays the groundwork for smarter, more strategic retirement moves.

In the sections ahead, we’ll explore Roth IRA basics, contribution rules, investment options, and withdrawal strategies—all designed to help you make the most of this tax-advantaged vehicle.

Explore the official IRS breakdown for more details:

Understanding the Basics of Roth IRAs

Definition and core features

At its core, a Roth IRA is an individual retirement account that allows you to invest after-tax income, meaning you pay taxes up front rather than later. So, what is a Roth IRA in practical terms? It’s a tool for achieving tax-free growth and tax-free withdrawals in retirement—assuming certain conditions are met.

Unlike traditional IRAs, contributions to a Roth IRA are not tax-deductible. However, the tradeoff is that you won’t owe taxes when you withdraw your earnings, provided your account has been open for at least five years and you’re age 59½ or older.

In addition, there are no required minimum distributions (RMDs), giving you more control over your retirement funds. This makes it an appealing choice for long-term investors seeking flexibility and future savings power.

For a deeper breakdown of Roth IRA features, visit Fidelity’s official guide:

How Roth IRAs differ from Traditional IRAs

Understanding the difference between a Roth IRA and a Traditional IRA is essential for choosing the right retirement strategy. While both are individual retirement accounts, they handle taxes in opposite ways.

With a Traditional IRA, contributions are often tax-deductible, but withdrawals in retirement are taxed as income. In contrast, a Roth IRA requires you to contribute after-tax dollars, yet allows for tax-free withdrawals later—especially valuable if you expect to be in a higher tax bracket during retirement.

Another key distinction is required minimum distributions (RMDs). Traditional IRAs mandate RMDs starting at age 73, whereas Roth IRAs have no such requirement, offering more flexibility and control.

Ultimately, choosing between the two depends on your current income, future tax expectations, and long-term financial goals.

Table: Roth IRA vs. Traditional IRA: A Side-by-Side Comparison

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax Treatment | After-tax contributions; tax-free withdrawals | Tax-deductible contributions; taxed withdrawals |

| Withdrawal Rules | Tax-free after age 59½ + 5 years | Taxed as income after age 59½ |

| RMDs | None | Begin at age 73 |

| Contribution Limits (2025) | $7,000 ($8,000 if 50+) | $7,000 ($8,000 if 50+) |

| Income Limits | Yes; phased out at higher incomes | No income limit to contribute |

| Tax Deduction | Not deductible | Fully or partially deductible |

Key tax advantages explained

One of the biggest draws of a Roth IRA is its array of tax advantages that compound over time. Here’s what makes it a standout:

Tax-free growth on all investments, including dividends, interest, and capital gains

Tax-free withdrawals in retirement if you’re age 59½ and meet the five-year rule

No taxes on qualified distributions—ever

No required minimum distributions (RMDs), unlike a Traditional IRA

No tax impact from internal account growth or rebalancing

Ideal for those expecting a higher tax bracket in retirement

Compound interest grows more efficiently without tax drag

Ultimately, a Roth IRA offers unmatched flexibility and long-term tax-exempt income—especially for younger investors or those planning early retirement.

Explore Vanguard’s breakdown of Roth IRA tax benefits:

Eligibility requirements

To contribute to a Roth IRA, you must meet specific eligibility requirements based on your modified adjusted gross income (MAGI) and tax filing status. Unlike employer-sponsored plans, eligibility depends entirely on your income and earned wages.

You must have earned income, such as wages or self-employment earnings, to qualify. For the 2025 tax year, single filers can contribute the full amount if their MAGI is below $146,000, with a phase-out ending at $161,000. Married couples filing jointly can contribute fully with a MAGI under $230,000, phasing out at $240,000. If your income exceeds these limits, a Backdoor Roth IRA may still provide access.

There are no age limits to contribute, unlike Traditional IRAs, which cap contributions once you reach 73.

“If you earn income and fall within IRS limits, you can unlock the tax-free power of a Roth IRA.”

Checkout Investopedia’s guide on Roth IRA contribution limits:

👉 Investopedia: Roth IRA Contribution Guide

Opening and Contributing to a Roth IRA

Finding the right financial institution

Choosing the right provider to open your Roth IRA is just as important as contributing to it. Not all financial institutions are created equal, and the one you choose will impact your fees, investment options, and user experience.

When evaluating where to open your Roth IRA, consider the following:

Low or no account fees to avoid unnecessary costs

Wide range of investment choices like ETFs, stocks, and mutual funds

Easy-to-use online platform or mobile app

Strong customer support and educational resources

Robo-advisor vs. DIY investing, depending on your comfort level

Top-rated institutions include Vanguard, Fidelity, Charles Schwab, and Betterment, all offering competitive Roth IRA solutions tailored to different investor needs.

Compare leading Roth IRA providers via NerdWallet’s in-depth guide:

Required documentation and process

Opening a Roth IRA is a relatively simple process, but having the proper documents on hand can make everything move faster. To begin, most financial institutions offer a seamless online application process that takes less than 15 minutes.

First, you’ll need a government-issued ID, your Social Security number, and bank account details to fund the account. Next, be ready to provide basic employment and income information, along with your contact details and beneficiary preferences.

Once submitted, your application will go through a quick verification process. Typically, approval happens within 24 to 48 hours. After approval, you can fund your Roth IRA, set up automatic contributions, and choose your investments based on your risk tolerance and retirement goals.

Want to see a sample checklist? Bankrate offers a helpful Roth IRA setup guide:

Contribution limits for different age groups

Contribution limits for a Roth IRA are set annually by the IRS and vary based on your age. As of 2025, individuals under age 50 can contribute up to $7,000 per year. However, those age 50 and older are allowed an additional $1,000 catch-up, raising their limit to $8,000 annually.

This age-based increase is designed to help late starters boost their retirement savings. Keep in mind, your contribution cannot exceed your total earned income for the year. So if you only earned $5,000, that becomes your maximum allowable contribution—regardless of your age bracket.

Also, remember that income limits still apply and can affect how much you’re eligible to contribute.

Q: Can I contribute the full amount if I only work part-time?

A: Yes, as long as your earned income meets or exceeds your contribution. For example, earning $7,000 lets you contribute $7,000.

Check the IRS for current Roth IRA contribution thresholds.

👉 IRS Roth IRA Contribution Limits

Income limitations and phase-out ranges

Alongside age-based contribution limits, your eligibility to fund a Roth IRA also hinges on your modified adjusted gross income (MAGI). Each tax year, the IRS publishes income ranges that determine your contribution status.

Table: 2025 Roth IRA Income Limits and Phase-Out Ranges by Filing Status

| Filing Status | Full Contribution If MAGI ≤ | Phase-Out Range | No Contribution If MAGI ≥ |

|---|---|---|---|

| Single | $146,000 | $146,001 – $161,000 | $161,000 |

| Married Filing Jointly | $230,000 | $230,001 – $240,000 | $240,000 |

| Married Filing Separately | N/A | $0 – $10,000 | $10,000 |

If your income falls within a phase-out range, your allowable contribution is reduced. Above the limit, consider a Backdoor Roth IRA strategy.

Use IRS guidance to calculate your exact contribution eligibility.

Deadline rules for annual contributions

When it comes to timing, the IRS offers flexibility for making Roth IRA contributions. Specifically, you can contribute up until the tax filing deadline—normally April 15 of the following year.

For example, for the 2025 tax year:

📅 Start Date: January 1, 2025

📅 End Date: April 15, 2026

🕒 Time to Contribute: 15.5 months

This extended window gives you time to evaluate income, tax brackets, and contribution strategies—even after the calendar year ends. Just be sure to indicate which tax year your contribution applies to if contributing early in the new year.

Most providers prompt you to select the tax year at the time of funding to avoid errors.

👉 IRA Contribution Deadlines: Key Dates to Maximize Your Retirement Savings

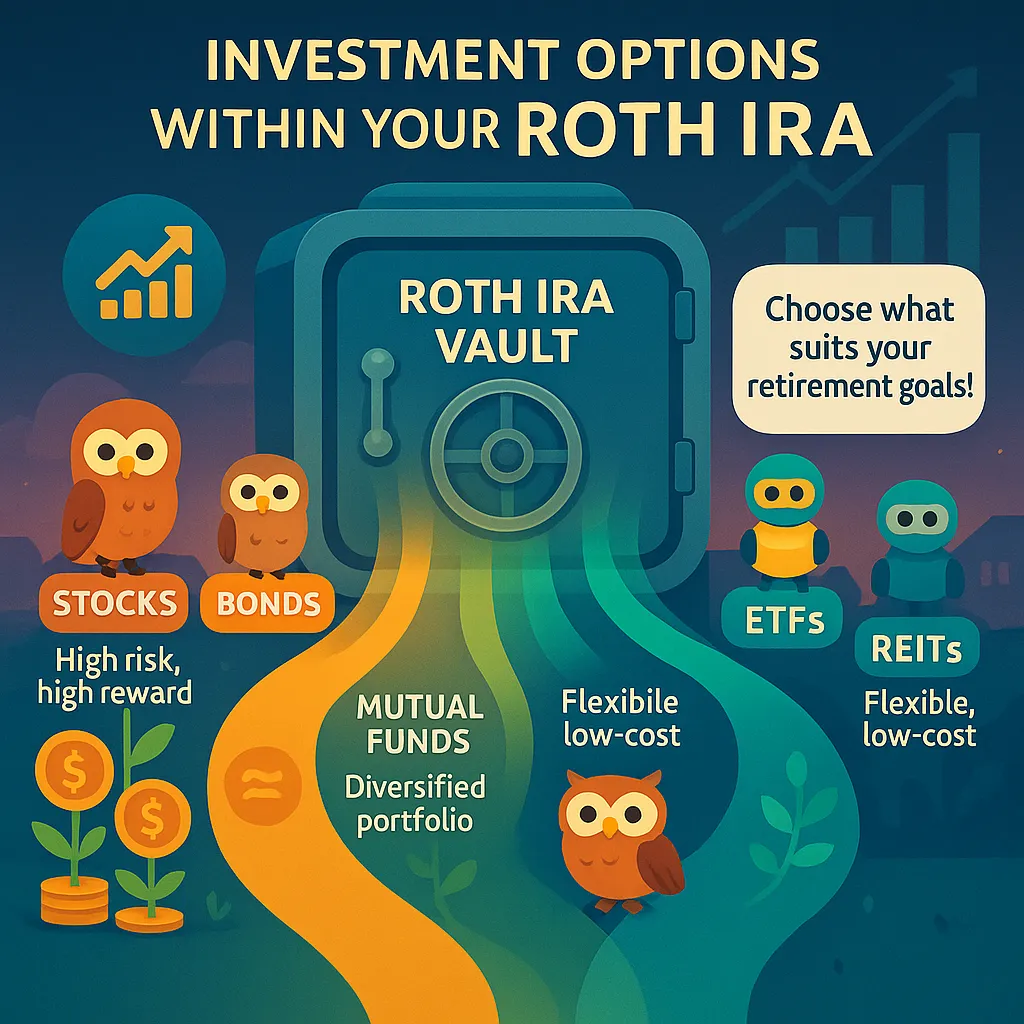

Investment Options Within Your Roth IRA

Common investment vehicles (stocks, bonds, ETFs)

Once your Roth IRA is open, the next step is choosing how to invest the money. Unlike savings accounts, Roth IRAs are not investments themselves—they’re vehicles that hold a mix of investment assets.

📈 Stocks: Offer higher growth potential but come with increased volatility. Ideal for long-term investors seeking capital appreciation.

📊 ETFs (Exchange-Traded Funds): Diversified, low-cost, and flexible. They track indexes or sectors and are perfect for hands-off investing.

💵 Bonds: Provide more stability and consistent income. Good for risk-averse investors or those closer to retirement.

Generally speaking, a smart portfolio includes a mix of these to balance growth and security. Your age, risk tolerance, and time until retirement should guide your asset allocation.

Explore how different assets shape your Roth IRA’s long-term performance.

👉 Morningstar on Roth IRA Investments

Alternative Investment Vehicles (Crypto, Forex)

While traditional assets like stocks and bonds dominate most Roth IRAs, some investors are exploring alternative investment vehicles—particularly cryptocurrency and foreign exchange (Forex).

🚀 Crypto (e.g., Bitcoin, Ethereum): Offers high-growth potential but comes with extreme volatility. To include crypto in your Roth IRA, you’ll need a self-directed Roth IRA (SDIRA) that allows non-traditional assets.

💱 Forex (Foreign Exchange): Involves trading global currencies. It’s high-risk, complex, and requires a self-directed account. Most standard IRA custodians don’t offer direct Forex access.

That said, these options are best for experienced investors with a high risk tolerance. Keep in mind, the IRS has strict rules about holding unconventional assets, and fees can be significantly higher.

Learn what it takes to include crypto or Forex in a Roth IRA responsibly.

👉 Can You Trade Forex in a Roth IRA?

👉 Can You Hold Crypto in a Roth IRA? Rules, Risks, and Benefits Explained

BONUS: Learn about Fidelity’s Crypto Roth IRA Account

Growth potential comparison

When evaluating growth potential within a Roth IRA, it’s essential to understand how different assets can impact long-term returns. Because Roth IRAs grow tax-free, choosing investments with strong compounding power can significantly enhance your retirement savings.

Stocks generally offer the highest long-term return potential but come with more volatility. They’re ideal for investors with longer time horizons and a higher risk tolerance. ETFs, which often track broad market indexes, offer diversified exposure with moderate growth and lower risk than individual stocks. Bonds, on the other hand, are more stable but deliver lower returns, making them more suitable for capital preservation and income generation.

In contrast, alternatives like crypto may offer explosive growth, but with unpredictable risk and limited IRA access.

Ultimately, a Roth IRA thrives when fueled by assets with long-term growth potential, carefully balanced with your age and risk profile.

See how a Roth IRA can grow over time:

👉 How Does a Roth IRA Grow? Tax-Free Compounding Explained

Risk management strategies

Managing risk inside a Roth IRA is just as critical as pursuing strong returns. Since you’re contributing after-tax dollars, protecting gains ensures you fully capitalize on the account’s tax-free growth potential.

Here are key strategies to manage risk effectively:

Diversify across asset classes (stocks, bonds, ETFs) to avoid overexposure

Adjust your asset mix based on your time horizon—more stocks when young, more bonds as you near retirement

Rebalance regularly to maintain your target allocation as markets shift

Use dollar-cost averaging to reduce timing risk by investing consistently

Match your risk tolerance to your investment choices, not someone else’s

Ultimately, risk management inside a Roth IRA means staying intentional—not reactionary—especially in volatile markets.

Learn how to balance risk and return in your Roth IRA.

👉 SoFI: Investment Risk Management

Maximizing the Benefits of Your Roth IRA

Compound growth advantages

What sets the Roth IRA apart from other retirement accounts is its unmatched ability to amplify returns through compound growth—without the burden of annual taxes. Over time, this advantage can dramatically elevate your retirement portfolio.

Your contributions generate earnings, and those earnings begin producing gains of their own. Since there are no taxes on interest, dividends, or capital gains, more of your money stays invested and working for you. This uninterrupted growth cycle becomes even more powerful when you start early and remain consistent.

Additionally, because Roth IRAs allow for tax-free withdrawals in retirement, you get to keep every cent of what your investments earn.

“The longer your money stays invested in a Roth IRA, the more powerful compound growth becomes—completely tax-free.”

Harness tax-free compounding for serious Roth IRA growth.

👉 The Magic of Compound Interest

Tax-free withdrawal strategies

With a Roth IRA, not only does your money grow tax-free, but qualified withdrawals are also completely tax-exempt—if you follow the proper strategy. Understanding the rules helps you maximize every dollar in retirement.

To make a qualified withdrawal, your account must be open for at least five years, and you must be age 59½ or older. However, there are exceptions that allow earlier, penalty-free withdrawals under specific conditions.

Here’s a quick breakdown:

Table: Roth IRA Withdrawal Rules: Tax-Free and Penalty-Free Exceptions Explained

| Withdrawal Type | Tax-Free? | Penalty-Free? | Conditions |

|---|---|---|---|

| After age 59½ (5-year rule met) | Yes | Yes | Qualified withdrawal |

| First-time home purchase | Yes | Yes | Up to $10,000 lifetime limit |

| Disability | Yes | Yes | Must be certified |

| Higher education expenses | No | Yes | Earnings taxed, principal penalty-free |

| Before age 59½ (non-qualified) | No | No | 10% penalty + taxes on earnings |

Learn how to make tax-free withdrawals the smart way.

👉 Schwab: Roth IRA Withdrawal Rules

Estate planning benefits

Beyond retirement income, a Roth IRA serves as a powerful tool in estate planning. Unlike Traditional IRAs, Roth IRAs are not subject to required minimum distributions (RMDs) during the account holder’s lifetime. This allows your investments to grow tax-free for as long as you live, maximizing the wealth you can pass on.

💼 $0 RMDs during your lifetime means more time for tax-free compounding

🧾 10-year withdrawal rule applies to most non-spouse beneficiaries under the SECURE Act

💸 $0 taxes on qualified withdrawals for heirs—preserving more of your legacy

Because Roth IRAs don’t generate taxable income for heirs, they’re an excellent way to reduce estate tax impact and keep inherited wealth intact. For families planning long-term, this account structure offers simplicity, growth, and tax efficiency.

See how Roth IRAs can strengthen your estate plan.

👉 Fidelity: Roth IRAs and Estate Planning

Using a Roth IRA for retirement income

Unlike most retirement accounts, a Roth IRA offers unmatched flexibility for generating tax-free retirement income. Because withdrawals aren’t taxed, you can strategically use your Roth IRA without increasing your taxable income or triggering higher Medicare premiums or Social Security taxes.

This makes a Roth IRA an ideal source for bridging income gaps, reducing your overall tax liability, or covering emergency expenses without penalty. It also pairs well with Traditional IRAs or 401(k)s, allowing you to stagger withdrawals and control your taxable income across retirement phases.

With no required minimum distributions (RMDs), you decide when to withdraw—and how much.

Q: Should I use my Roth IRA first or last in retirement?

A: Many planners recommend using it last to let it grow longer, but the best approach depends on your tax bracket and total income mix.

Explore how to use a Roth IRA for efficient retirement income.

👉 SmartAsset: Roth IRA Withdrawal Strategies

Rules for Withdrawals and Distributions

Qualified vs. non-qualified distributions

Understanding the difference between qualified and non-qualified distributions is crucial for maximizing the tax-free benefits of a Roth IRA. A qualified distribution occurs when your account has been open for at least five years and you are age 59½ or older. These withdrawals are completely tax- and penalty-free.

In contrast, non-qualified distributions happen when you withdraw funds before meeting those two key conditions. Contributions can always be withdrawn tax-free, but earnings may be taxed and penalized.

Here’s a quick breakdown:

Table: Roth IRA Distribution Rules: Qualified vs. Non-Qualified Withdrawals Explained

| Type of Distribution | Account Age ≥ 5 Years | Age ≥ 59½ | Taxed? | 10% Penalty? |

|---|---|---|---|---|

| Qualified | Yes | Yes | No | No |

| Non-Qualified (No Exceptions) | No/Yes | No/Yes | Yes (on earnings) | Yes (on earnings) |

| Non-Qualified (With Exceptions) | Varies | Varies | Possibly | No |

The five-year rule explained

The five-year rule is a critical part of Roth IRA withdrawal strategy. It determines whether your earnings can be withdrawn tax- and penalty-free. What many people miss is that there are actually two different five-year rules depending on how and when funds were added to the account.

For regular contributions, the clock starts on January 1 of the tax year in which you made your first Roth IRA contribution. This applies to determining whether future withdrawals are qualified—meaning you’ve met the age 59½ requirement and held the account for at least five years.

For Roth conversions, each converted amount has its own five-year clock to determine whether the converted principal can be withdrawn without a penalty—even if you’re over 59½.

Understanding these timelines can help you avoid taxes and penalties while preserving your Roth IRA’s tax-free status.

Understand the timing to maximize tax-free Roth withdrawals.

👉 Fidelity: Roth IRA 5-Year Rules

Early withdrawal penalties and exceptions

Withdrawing from a Roth IRA before meeting qualified distribution rules—either being under age 59½ or not satisfying the five-year rule—can trigger taxes and a 10% early withdrawal penalty on your earnings.

However, your contributions (what you originally put in) can always be withdrawn tax- and penalty-free at any time. It’s only the earnings portion that’s subject to taxation and penalties if pulled early.

That said, the IRS allows several exceptions to the penalty:

First-time home purchase (up to $10,000)

Qualified education expenses

Disability

Unreimbursed medical expenses exceeding 7.5% of AGI

Health insurance premiums while unemployed

Substantially equal periodic payments (SEPP)

Knowing these exceptions can help you use your Roth IRA more flexibly—without undermining its long-term benefits.

Learn when early withdrawals can be made penalty-free.

👉 IRS: Roth IRA Early Withdrawal Exceptions

Required minimum distribution differences

One of the most appealing benefits of a Roth IRA is that it has no required minimum distributions (RMDs) during the account holder’s lifetime. This sets it apart from Traditional IRAs, which mandate RMDs starting at age 73.

📆 RMD Age for Traditional IRA: 73

🚫 RMDs for Roth IRA Owners: None during lifetime

📈 Growth Duration: Unlimited, tax-free, for Roth IRA holders

Because Roth IRAs don’t force withdrawals, your money can stay invested and compounding tax-free for as long as you wish. This flexibility is a strategic advantage for retirement planning and legacy building.

However, under the SECURE Act, non-spouse beneficiaries must withdraw inherited Roth IRAs within 10 years—though those withdrawals remain tax-free if the account was qualified.

See how Roth IRAs help you sidestep mandatory withdrawals.

👉 Do Roth IRAs Have Required Minimum Distributions? What You Need to Know

Advanced Roth IRA Strategies

Roth conversion tactics

A Roth conversion allows you to move money from a Traditional IRA or 401(k) into a Roth IRA, paying taxes upfront in exchange for tax-free withdrawals in retirement. This tactic is especially useful if you anticipate being in a higher tax bracket down the road.

You’ll owe income taxes on the converted amount in the year of the transfer, so timing is key. Many investors take advantage of low-income years, early retirement, or years with significant deductions to minimize the tax hit.

A smart strategy is to do a partial Roth conversion, breaking up large transfers over several years to avoid crossing into higher tax brackets.

One caveat: converted funds must remain in the Roth IRA for five years to avoid penalties—even if you’re over 59½.

Explore how strategic conversions can boost your tax-free retirement income.

👉 The Three Tests Before a Roth Conversion

Backdoor Roth IRA method

The Backdoor Roth IRA is a smart, legal workaround for high-income earners who exceed the IRS limits for direct Roth IRA contributions. It involves two steps:

Make a non-deductible contribution to a Traditional IRA using after-tax dollars

Convert that contribution to a Roth IRA—usually immediately, to avoid gains

Why it works:

Bypasses Roth income limits

Takes advantage of Roth’s tax-free growth

Keeps your retirement strategy IRS-compliant

Important considerations:

If you have other pre-tax IRA balances, the pro-rata rule could trigger unexpected taxes

You must report the transaction using IRS Form 8606

Timing the conversion quickly helps avoid complications from gains

Used correctly, the Backdoor Roth opens tax-free retirement benefits to those who would otherwise be ineligible.

Unlock Roth IRA access with the backdoor strategy.

👉 Vanguard: Backdoor Roth IRA Guide

Mega backdoor Roth opportunities

The Mega Backdoor Roth is a powerful strategy for high-income earners who want to contribute far more to a Roth IRA than standard IRS limits allow. It works through your 401(k) plan, using after-tax contributions and rollovers.

First, you contribute up to the regular 401(k) limit—$23,000 in 2025, or $30,500 if you’re 50 or older. Then, you make additional after-tax contributions, bringing your total up to the full 401(k) cap of $69,000 for the year. From there, you roll those after-tax funds into a Roth IRA or Roth 401(k) for long-term, tax-free growth.

“The Mega Backdoor Roth turns your 401(k) into a Roth IRA funding powerhouse—if your plan allows it.”

Not all employers offer this flexibility, so review your plan carefully before implementing.

Leverage your 401(k) to supercharge Roth IRA contributions.

👉 Forbes: Mega Backdoor Roth Guide

Spousal Roth IRA benefits

A Spousal Roth IRA allows a working spouse to contribute on behalf of a non-working or low-earning spouse, helping both partners build tax-free retirement savings—even if only one earns income.

To qualify, couples must file a joint tax return, and the working spouse’s earned income must equal or exceed the total IRA contributions. In 2025, this means up to $14,000 for couples under 50, or $16,000 if both are 50+.

Here’s a quick snapshot:

Table: Spousal Roth IRA Contribution Limits and Eligibility Requirements for 2025

| Spouse | Contribution Limit (2025) | Eligibility |

|---|---|---|

| Working Spouse | $7,000 ($8,000 if age 50+) | Must have earned income |

| Non-Working Spouse | $7,000 ($8,000 if age 50+) | Must file jointly with working spouse |

This strategy helps stay-at-home spouses grow wealth, gain retirement independence, and benefit from Roth IRA tax advantages.

Help your partner grow retirement savings—Roth style.

👉 Nerdwallet: Spousal IRA Guide

Roth IRA laddering technique

The Roth IRA laddering technique is a strategic way for early retirees to access funds before age 59½—without paying penalties or taxes on earnings. It takes advantage of the five-year rule for Roth conversions and spreads withdrawals over time.

Here’s how it works:

Convert a set amount from a Traditional IRA or 401(k) to a Roth IRA each year

Wait five years after each conversion to withdraw that amount penalty-free

Continue the process annually to create a “ladder” of accessible funds

Use the converted funds to bridge income needs before other retirement income kicks in

This method provides early access to tax-free income while preserving your long-term investments and avoiding early withdrawal penalties.

Build a tax-free income stream—year by year.

👉 How a Roth IRA Conversion Ladder Works

Final Thoughts

The Bottom Line: Why a Roth IRA Could Be Your Best Retirement Bet

When it comes to long-term financial freedom, few tools offer the tax advantages, flexibility, and control of a Roth IRA. From tax-free growth and penalty-free withdrawals to advanced strategies like conversions, backdoors, and laddering, this account adapts to every phase of your retirement journey.

Unlike traditional retirement accounts, a Roth IRA lets you grow wealth tax-free, avoid RMDs, and even leave a legacy with minimal tax impact. Whether you’re just getting started or optimizing a multimillion-dollar portfolio, the Roth IRA delivers unmatched versatility.

The bottom line? The earlier and more intentionally you use it, the greater the payoff.

👉 Want more tips like this? Check out the latest on the Investillect blog.